Before or After the Storm: Inflation, Energy Prices and Recessions

Roundtable Discussion at Tusvanyos Summer University

This week’s column is a bit different. It’s the written version of my Roundtable Discussion at Tusvanyos Summer University, 21 July 2022, Tusnad, Romania

You might be able to watch the panel, it’s Thursday, July 21, at 9:30 AM (Romanian time): https://www.tusvanyos.ro/en/

Roundtable panelists

Varga Mihály, Finance Minister, Hungary

Teleki Gábor, Managing Director, Gedeon Richter Farmacia Rt. and Pharmafarm Rt.

Christopher P. Ball, Director, Central European Institute, Quinnipiac University

Cseke Attila, Minister of Development, Public Administration and Public Works, Romania

Moderator: Mátis Jenő, Transylvanian Hungarian National Council, Economist and Vice-President responsible for the Central-Transylvania region

Before or after THE storm. What storm?

Many call everything today a “perfect storm”. There is indeed some perfect coincidence of insane events shaking the world today. Economically we’ll focus on inflation, energy prices and recessions, but there is a general malaise out there that is weighing on everyone.

As the representative American on the panel, I’ll talk about global economic issues with a focus on the US.

Inflation

Let’s start with inflation.

Globally, inflation today is around 9%. The US inflation rate is 9.1%, the Euro Zone rate is 8.6%, and in the UK it’s 9.1%.

Asian inflation is a bit lower, but not much. Australia has 5.1%, New Zealand has 6.9%, South Korea 6%, and Japan – which is the anomaly – only has 2.5%. China reports 2.5% inflation but who knows.

In the central and eastern European region, inflation is higher: Hungary has 11.7%, Romania 15%, then Poland has 15.5%, Czech 17.2% and Slovakia with that strong Euro has 13.2%.

There is a lot of variation across the Eurozone generally as well. Germany has 7.6% and it’s 5.8% in France. That Germany has any inflation and that it’s worse than French inflation is quite surprising in its own right when you think about it. Italian inflation is 8%, about the same as Portugal at 8.7%. But then Spain has 10%, Greece 12.1% and of course Slovakia, again, is at 13.2%.

I’ll leave it up to the Europeans on the panel to discuss European inflation and I’ll turn instead to US inflation.

US Inflation

Let’s start by only looking at the period before war broke out in the Ukraine in March this year.

From 2010 to 2020, the US inflation rate averaged around 2% annually. The same was true in the Eurozone as well, by the way. There was a general belief among central bankers around the world, and definitely at the US central bank (“the Fed”), that we had essentially conquered inflation. By cleverly manipulating interest rates they felt they could control inflation quite well.

I believe that was a bit delusional and there are many reasons to be skeptical, but it was the dominant view nonetheless.

In any case, the Covid pandemic hit. People stayed home – by choice and by force – businesses closed and the world turned upside down. As we all remember.

Prices dropped for some goods and shot up for others. Companies and the network of companies – the so-called supply chain of goods around the world – struggled to adjust.

It’s hard to convert the production and supply of everything overnight. And it was also hard to know how much to invest in doing so since no one knew how long Covid and lockdowns would last.

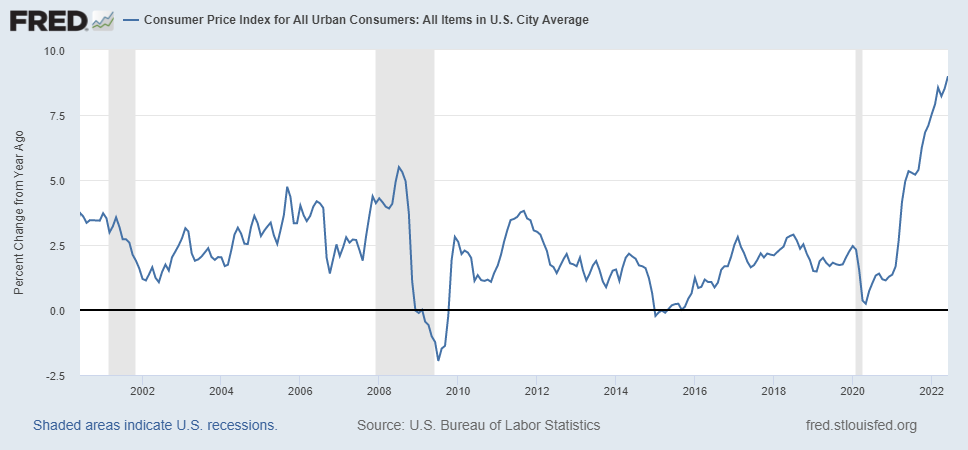

US Inflation in 2021

If you simply look at US inflation (see graph), it’s clear that in 2021 it looked like inflation was returning to its pre-Covid 2-2.5% level, maybe a little higher as we adjust back to normal, but nothing too concerning.

By summer 2021, however, US inflation was running around 5%. The Fed should have started to respond then. It did not.

By Fall, US inflation was running above 5% and ended the year at 7%. The US Fed definitely should have responded by then. It still did not.

The US started 2022 with inflation at 7% and it has been rising ever since.

Inflation started in the USA in 2021 which means that whatever caused inflation probably happened in 2020.

Causes of US Inflation: The War In Ukraine

Today, energy price inflation in the US is about 40% a year. Food price inflation is around 10%. Services inflation is around 6%. So it’s easy to think that the overall 9.1% inflation number is being driven by energy prices. It’s only a small step from there to blame the war in Ukraine.

Clearly the war is causing a spike in energy prices as world supplies re-adjust. This is especially true in Europe which is reliant on Russian energy, but I’ll leave that discussion for the other panelists.

The problem with this argument for US inflation is that energy inflation in the USA was already 30% by the end of 2021, well before the war in Ukraine. At most then, the war in Ukraine added another 10% (or 1/4th of the current 40% energy inflation), but still doesn’t account for the bulk of energy inflation in the USA.

And, if you exclude energy (and food), core inflation is still about 6%. So, at most you can argue that about 30% of the 9.1% inflation (i.e., 3 of the 9 percentage points) comes from energy (and food) and of that, only 1/4th, or .75 of a percentage point, from the Ukraine war. There is simply no sense in which the war in Ukraine is driving US inflation today.

The war in Ukraine certainly makes inflation worse but it’s not the cause.

Government Spending and Money Printing

The most obvious cause of inflation in the United States today is the excessive government spending combined with excessive money printing in 2020 and 2021.

During the Great Financial Recession of 2008/2009, the US grew government spending by about 10% a year. Money growth averaged 8% in 2009 and 2.5% in 2010. Inflation surged to 3.8% in 2011 but fell consistently after that.

During Covid we increased government spending by 50% in 2020 and again by 44.4% in 2021. Money grew by about 25% in 2020 and 16% in 2021.

One minor point that’s often overlooked with this sort of unique back-to-back shock is that it adds up (actually multiplies up, compounding over time). That is, by end of 2021 government spending had increased 116% and money had increased by 45% compared to 2019. That’s a lot by any measure.

To put that in perspective, historically money grew on average about 7% a year in the USA. That is, since the 1940s. Money growth got out of control and hit 10-13% a year a few times in the 1970s which led to our first double digit inflation since the World Wars.

Long and Varied Lags

Traditional monetary theory says a massive and sustained increase in the money supply takes about 6-18 months to feed into inflation.

We started printing at a rate of over 20% a year by summer 2020. 12 months later we started seeing an increase in inflation. Some of that may of course be coincidence since Covid lockdowns came and went, etc. But the timing is still suspicious.

We kept printing money at over 20% until March 2021. In March we were still printing at 24%, the highest rate in the entire history of the US Fed’s existence!

At the beginning of this year, 2022, we were printing at about a 13% annual rate. That’s the rate at which we were printing in the 1970s. By May we finally lowered it to a 6% annual growth rate.

That much money for that long is like a tidal wave of money flooding the economy. Sure, where there are bottlenecks – like with energy – there will be a bigger flood, but there will be a general flood in any case. That seems to be the best explanation of the inflation. Tons of money gushing into the economy at completely unprecedented rates for two solid years.

Most countries experiencing inflation today did something similar during Covid.

I am not a politician, but at least in the USA I wish our political leaders would just stand up and admit it. “Yes, we were all scared during Covid. It was by far the biggest single hit to our economies since the Great Depression. We needed to spend and print money to keep the system intact. Now we’re paying the price in terms of inflation. But at least we are here with a functioning economy. So let’s suck it up and work through this inflation together. We are Americans!”

But no, we all blame each other. Blame Putin. Blame businesses. Republicans blame Democrats. Democrats blame Republicans. And it’s an election year in the US, so it’s going to continue to be political chaos.

If there really is a 6-18 month lag, then we ended the extreme massive money printing last year and the excessive money printing this year. So, the massive inflation should be hitting this Fall into Winter and then we’ll have high inflation through next year and it’ll subside from there.

Recessions

I think we are already in a recession of sorts in the USA and that the hard, truly painful part is just starting now.

US GDP growth was negative in Q1 and is expected to be negative in Q2. We are already seeing spending slow and real wages have been declining by about 3% a year now for a while. That’s painful.

The odd thing is that the flood of money, the government stimulus and the lockdowns meant that Americans acquired a lot of savings that they are still spending it down. That’s keeping demand stronger than it would otherwise be while at the same time, people are worse off by the month due to inflation and you see it in opinion data.

Consistently all the data shows that Americans – and most people around the world – feel frustrated. They feel like they are constantly falling behind, struggling to pay their bills and worrying about the future. I get it. We all feel it.

Whether that’s officially a recession yet or not, I don’t know. In the US, the National Bureau of Research categorizes recessions and they use a wide range of measures.

But the name “recession” is irrelevant to the average person. These are hard financial times. We just came out of Covid and hoped to see brighter skies. Instead we can’t buy groceries and pay our rent. This is hard and painful and we all feel that pain.

Interest Rates Rising and More Pain

And now the US Fed is finally raising interest rates to fight inflation. I think this is about a year too late. In my opinion the US Fed should have reduced the growth of the money supply dramatically last summer and slowly raised the interest rate as well.

Had we started slowing money growth a year ago we might have managed a relatively soft landing. But they didn’t.

So now they are trying to catch up and raising rates rapidly.

In March – MARCH! – the Fed’s policy rate was still nearly zero, at 0.8%. They raised it 3 times since then and it’s now at 1.6%. They will raise it again in July by .75 to 1% so we’ll be over 2% by August. This raises all interest rates in the economy.

Nominal interest rates should be around the level of inflation plus a little more.[1] If inflation is going to be between say 6 and 10% over the coming year or so in the US, then the Fed’s rate should be around the same. We have a long way to go from 2%. Probably we’ll get it around 4-5% by spring or early summer and stop. That’s just a guess at this point, but it seems reasonable.

The problem is that higher interest rates are part of the medicine of fighting inflation but they are painful. American households are seeing credit card rates rise, auto loan rates rise, student loan rates rise, housing loan rates rise and so on. That hurts.

American businesses see loans, capital financing, payroll financing and all other financing getting more expensive. Banks raise rates, lend more cautiously and businesses take fewer risks. Overall things contract but in the most painful way possible.

And those in the lowest income categories and those with fixed incomes are hit hardest by both inflation and higher interest rates. These times will be hard and I believe they’ll be hard for the coming year for sure.

And that’s just domestically. It doesn’t even capture the global effects of both the US actions and the effects of the global recession on the US economy.

Global Effects

First, most countries are facing the same inflation challenges. As a result most households are feeling the same pain and most politicians are facing the same unhappy populations.

Most countries experienced lockdowns both by force and by choice. Most countries felt the supply chain shortages and the strange mass expenditure switching from services to goods to different goods and now back again. So the problems are very common across countries. … At least we are all in this together.

As central banks move to raise interest rates and fight inflation, local populations will all feel the same pain I described for the American households and businesses. These are tough times and they will remain for a while.

Then we have the unique position of the USA in the global economy. Because the US is a large player in most markets, is the world’s biggest reserve currency, and a global safe haven for investors, what happens in the US has an effect everywhere.

The US began raising interest rates late in my opinion, but still we raised them sooner than most other countries. As of today, the ECB still hasn’t raised rates! One effect of this is that the US Dollar has been strengthening against most other currencies in the world.

The strong dollar has several effects. First, it should make it easier to export to the US since non-US goods will be a bit cheaper for Americans to buy. That’s a little help to many economies. Second, however, it means many crucial items in the world like oil which is priced in US dollars, are even more expensive for all other countries. That means the energy crisis due to the war in Ukraine is amplified for everyone else in the world because they suffer both the shortages and resultant price hikes and they suffer from the rising cost due to a stronger dollar. And since energy is critical for everyone in an economy, both businesses and households, an energy price shock is a major negative shock to any economy.

The rising interest rates and the US being a safe haven at a time when most economies are faltering also means that the US interest rate policy is causing a sudden stop in capital flows to many markets. This drives up interest rates rapidly in markets that would not otherwise be raising rates yet. So this hits them hard.

Sudden stops alone drove waves of emerging market crises in the 1990s and early 2000s. This means the danger of a string of economic collapses and further contagion is high and getting higher. Sri Lanka’s collapse is important not because Sri Lanka’s economy is critical – although it is important and we should all feel for the Sri Lankan people – but because we all worry that it is the first in a coming string of collapses.

Those same pressures, along with the energy crisis, are causing complications in the Eurozone for Italy and likely Greece which may soon have debt financing problems as Euro and world interest rates rise.

Dangerous Times

These are dangerous times indeed. I think we are already slipping into a global recession. Inflation is at its highest in 40 years in many countries around the world. Poorer countries and poorer people are struggling the most and will continue to face food shortages and general economic malaise. It won’t be pretty and it won’t be easy.

I think the US is essentially in recession now. Europe may be as well, especially as the war in Ukraine continues. And we haven’t even discussed the hard consequences of the sanctions on Russia which are adding even more pain to everyone but are having questionable if any deterrent effects on Putin.

We are still trying to figure out the new, post-Covid landscape too. Unemployment seems crazy low everywhere – 3.6% in the USA – but no one believes those numbers. Well over a million people still haven’t returned to the labor force in the US. I’m sure the same is true in most countries.

Where are those people? I don’t know. Are they working online for foreign companies and not reporting their employment? Did they retire early? Will they ever come back?

I wouldn’t want to work at a central bank or a central statistical office these days. We need to rethink how we calculate a lot of our data. So much has changed and we still don’t understand it well.

Ending on a High Note

Despite all of this, I’m an optimist. The 1970s were a mess. Inflation was high. Unemployment was high. We had an energy crisis. But we came through.

The 1980s were good, the Soviet Union collapsed and the 1990s were pretty darn good overall. Tusvanyos started then in Balvanyos. I saw some of you there in the 90’s.

Hungary and Romania are much more prosperous today than they were then. Your countries and economies will weather this storm today better than you could have then.

The US is in a crisis economically, socially and psychologically. There’s nothing like some hardship to focus the mind and help us move past the superfluous and focus on the important things in life: our families, our faith, our friends.

This too shall pass. But it’s going to be a rough ride. We will come out the other side and, God willing, continue at least to meet here in Tusnad in the meantime.

Thank you.

[1] Technically, the nominal interest rate (i) equals the real interest (r) rate plus expected inflation (e_inf): i = r + e_inf.