Causes of (Dis)Inflation

Well… I got more emails and comments about my New Year’s Report on inflation around the world than I have in a long time.

I was surprised. Thank you!

Photo by Nathan Bingle on Unsplash

Everyone has a favorite theory or counterargument for what drove the rise and subsequent decline in inflation. Today I wanted to follow up and maybe shed light on a range of possible drivers of inflation based on some basic data.

This will just focus on the U.S. experience, but I do plan to conduct a similar experiment with as many countries as I can. When I do that I’ll share it as well.

To begin, I’ll state the rationale for each possible driver and link it broadly to an “economic school of thought”. This isn’t really a test of theories, however. This is an exploration of the data, possible causes, and more likely than not, it shows why simple tests of these theories prove elusive. I hope you find it interesting.

What to Look for

Our ideal case would be to identify something that clearly rises just before inflation picks up and then falls just before inflation falls. That’s at least a potential cause of both the rise and the fall in inflation.

There’s no real reason, however, to assume that the same thing drove both the increase and the decrease in inflation. Maybe a burst of spending drove inflation up and the Fed’s interest rate increases brought it down. So, the second thing we’ll look for is possible causes of the inflation and possible different causes of the disinflation.

Throughout we’ll keep a running tab of each variable we look at in terms of possibly driving both the increase and the decrease, or one, or the other, or neither, and then summarize them all at the end.

Schools of Thought

Broadly speaking there are three schools of thought on these topics in economics today. They are the money, the interest rate, and the fiscal schools. They are not at all mutually exclusive.

The money school is a bit old-fashioned in academic and policy circles, but still around for good reason. Generally, this school views too much money as driving inflation. Therefore, big increases in the money supply should drive inflation up and big decreases in the money supply should pull inflation down. We’ll look at M2 in the United States, a classic measure of the money supply.

The interest rate school has been the dominant one in academic and policy circles since the mid- to late-nineties. Generally, this school sees interest rates as controlling inflation through an inverse relationship. Higher interest rates lower inflation and lower interest rates raise inflation[1]. Therefore, a big decrease in interest rates should drive inflation up and a big increase should bring inflation down. We’ll look at the federal funds rate, the key policy interest rate for the U.S. Fed[2].

A big group in the interest rate school also relies on a Phillips Curve as a driver of inflation, which the central bank then curbs or enhances with interest rates. The Phillips Curve basically argues that lower unemployment drives up inflation and higher unemployment drives down inflation. After that so-called fundamental cause of inflation, the central bank fights that inflation by manipulating the interest rates. We’ll look at the unemployment rate.

The final and newest school in some sense is the fiscal school. This school generally thinks as follows. A nation’s money and its bonds are only as valuable as the government that issues them. Therefore, when people doubt the government’s future financial stability, they begin to value its money and bonds less, and this causes inflation. A sudden worsening of expected future government fiscal budgets can drive inflation up, and an improvement of those fiscal budgets can pull it down.

We’ll already be looking at money, M2, so we’ll also look at the change in government’s total debt which tells us about the bonds they had to issue. And, since this view is really focused on current beliefs about the future financial stability of the government, we’ll look at current government spending and also look at the Congressional Budget Office’s predictions about government finances going forward. This fiscal theory is in some ways the hardest to test empirically. Expectations and beliefs about things are notoriously hard to pin down with data.

All the graphs start in 2010 and include inflation. That way they are comparable. Also, 2010 is just after the Great Financial Recession and there are many reasons to believe monetary policy works differently since 2010. For each variable presented I evaluate whether it shows something that could have driven either the rise or the fall of inflation, or neither. Finally, I conclude with some comments.

My advice to readers: use your eyes; look at the graph. The red line is always inflation. Does the other line look like it could have pushed the red line at the beginning (around 2020) or the end mid-2022 to the end of the graph? My only caveat is that we expect the cause to move first. That is, the blue lines movement up/down should precede inflations rise/fall. Simultaneous movement usually indicates something else caused both lines to move.

Money and Inflation

This first graph looks at the annual percentage growth rate in the money supply (blue line), measured by M2, and inflation (the annual growth rate of the Consumer Price Index). Money was growing at about 5-10% per year until 2020, then spiked to 20-30% for 2020 and 2021. Sure enough, soon after inflation (red line) began to rise. Money growth slowed in 2022 and turned negative in 2023. Around that time inflation peaked and began to decline.

Evaluation: money growth could explain both the increase and the decrease in inflation.

Unemployment and Inflation

The unemployment rate (blue line) spiked during Covid in 2020, then returned to its trend level around 3-5%. An increase in unemployment should lower inflation and we actually see some fall in inflation immediately after 2020. But, unemployment falls consistently thereafter and while a major drop might raise inflation, this is a slow persistent decline throughout while inflation (red line) rose, peaked, and fell. There seems to be no relation at all between these.

If anything, you’d read this graph as the spike in unemployment in 2020 caused a later rise in inflation and unemployment’s decline thereafter led to a later fall in inflation. That is 100% the opposite of what the Phillips Curve predicts.

Evaluation: changes in unemployment do not seem likely to explain the increase or the decrease in inflation.

Interest Rates and Inflation

A drop in interest rates should raise inflation and an increase should lower inflation. We see a significant decrease in interest rates (blue line) in 2020 from around 1-2% to essentially zero where they stay until 2022. Inflation (red line) soon followed. And, interest rates rose in 2022, right at the peak of inflation. As interest rates rose dramatically from that point on, inflation also fell. Based on this graph alone, interestingly enough, after interest rates peaked and stayed constant around 5%, from mid 2023 onward, inflation too seems to have stopped falling and bounce around the 3-4% level.

Evaluation: changes in interest rates look like they could explain both the rise of inflation and the fall.

Government Spending and Inflation

From a fiscal perspective, higher government spending without any other change (like an increases in taxes to finance it) worsens the government’s budget situation and decreases the value of money issued by the government. The double hump increase in government spending (blue line) in 2020 and 2021 is indeed followed by inflation (red line). Government spending then looks like it returns to trend levels briefly, then rises again in 2022 and 2023 but inflation continues to decline.

One could argue here – and very validly so – that this one-time burst of spending led to a one-time burst of inflation. Both one-time bursts subsequently dissipated.

Evaluation: government spending looks like it could potentially explain the rise in inflation, but not inflation’s later decline. Unless you accept the one-time burst view, and then it explains both.

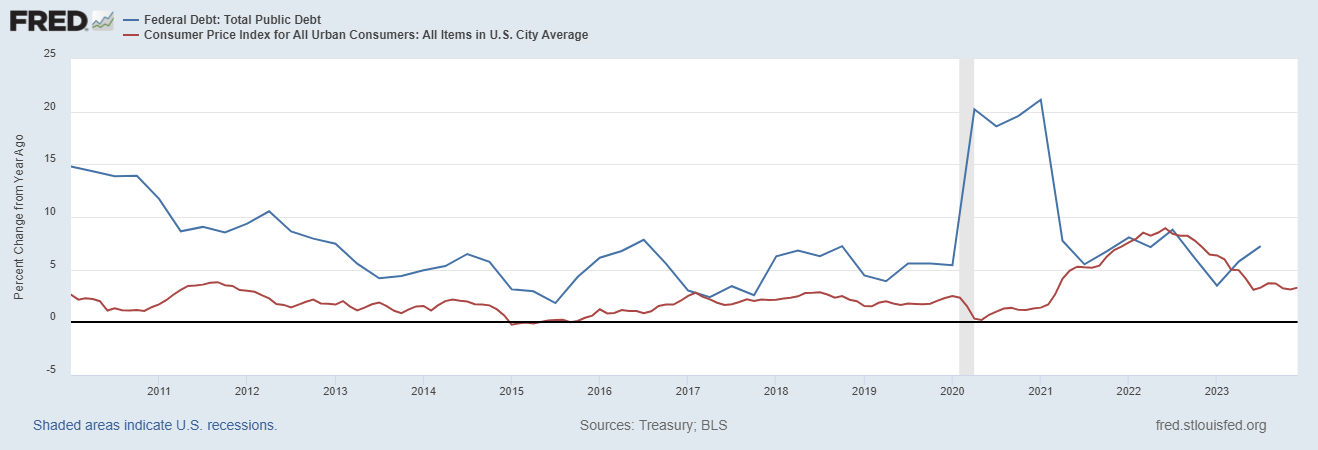

Government Debt and Inflation

Technically, the fiscal view argues that the over issuance of government liabilities, bonds and money, worsen the fiscal situation. They are the sources of funding and therefore reflect the big spending. As mentioned above, if it were financed by taxes, you wouldn’t need to borrow or print money to finance it. This graph reflects the, let’s say, poor financing choice of the government’s double hump spending in the previous graph.

The graph here shows the growth rate of government debt (blue line) and inflation (red line). Government debt was growing at around 5% pre-2020, then grew around 20% for two years, and fell thereafter. If the effect is delayed at all, then it could explain the rise in inflation. Again, however, we see it rising again in 2023 but inflation is falling.

Evaluation: the change in government debt looks similar to the government spending it was financings. That is, it too looks like it could potentially explain the rise in inflation, but not inflation’s later decline.

Expectations of Debt and Deficits and Inflation

Sorry to repeat, but once again, the fiscal view is really about people’s expectations of the government’s future fiscal situation. I have no good way to measure how people view the future. But we do have the U.S. government’s own prediction about its future financial situation. We can assume people are generally aware of this.

This pair of graphs is one I’ve shared before. It’s from the U.S. Government’s Congressional Budget Office’s (CBO) latest report, which was released in June 2023[3]. This looks bad indeed and, if right, predict an ever worsening government financial situation in the United States over the coming 20+ years.

If this plays any part in people’s valuation of the US dollar, it should be worsening our view of the dollar’s value. This information was known pre-Covid as well, however. This information is not new. Therefore we shouldn’t view this long-term perspective as driving inflation’s increase or decrease at all.

Page two of the 2019 CBO report[4] shows basically the same two graphs. The only difference is that in 2023 we are further along, and debt is higher than predicted in 2023. Perhaps the fiscal folk would argue that this information was revealed in 2020 and that drove the burst of inflation.

Evaluation: expectations of the future financial situation of the government doesn’t seem likely to have influenced inflation unless you think 2020 revealed to everyone that the fiscal situation was worsening more than they otherwise expected. In that case, it could conceivably have led to the burst of inflation. But we already saw that, and saw it more clearly so, from the burst of spending and change in debt.

A technical side: It’s interesting to note that the fiscal theories are usually defined in terms of the government’s primary deficit (literally income minus government expenditures) and not in terms of overall deficit (i.e., primary deficit plus interest expenses). The CBO’s note says explicitly, the primary deficit is 3% of GDP today and expected to be 3% of GDP in 2053 too. None of that’s good, but in strict fiscal theory terms it says there should be no expected change.

Conclusion

Just based on looking at pictures,

Money might explain both the increase and decrease in inflation

Interest rates might explain both the increase and decrease in inflation

Government spending and its financing (i.e., the change in the debt) might explain the increase but not the decrease in inflation. Or it’s a one-time burst and explains both.

The government’s future financial condition doesn’t seem to explain anything.

The unemployment rate doesn’t seem to explain anything.

Based on this sort of data, knowledge of what we all can remember happening, and on an understanding of basic economic theory, the U.S. inflation story looks pretty clear.

Covid hit. The U.S. government increased government spending, which it financed by printing money and issuing debt. Additionally, it lowered interest rates and printed additional money to ease liquidity conditions in markets. All of that hit the economy and generated inflation.

How high and how rapidly inflation rose was surely also influenced by the economy also struggling initially with some structural issues like supply-chains stopping, massive expenditure switching from goods and services to mostly goods, and labor shortages as everyone, who could, hid at home.

Subsequently, the government (the Fed) raised interest rates and reduced the money supply dramatically, and that led to a decrease in inflation.

That seems to be the key story, seems accurate, and borne out by the data presented here. I didn’t cherry pick any data, and used what should be the standard measures for everything. No tricks here. It’s pretty clear.

Several people emailed me about different factors and causes, and so on. I simply wanted to share here the main contenders and how they played out. I hope it was informative for you. The story seems straight forward and largely consistent with, let’s say, Macro Econ 101 economic theory: too much government spending and overprinting money caused inflation, reducing the amount of money and raising interest rates lowered it.

[1] The exact process driving this result can differ widely in these models making for a very wide range of models and theories that fit under this umbrella of “the interest rate school”. Actually, versions of the money and the fiscal schools’ theories fit under “interest rates” as well. Again, these are not mutually exclusive theories. Traditionally, money and interest rates were even just two different views of the same phenomenon.

[2] Technically, the Fed’s policy rate today is the interest paid on bank reserves, but then that is seen as immediately translating into the federal funds market, and hence the fed funds rate is still the one everyone watches.

[3] Here’s the link to the 2023 CBO report: https://www.cbo.gov/publication/59014

[4] Here’s the link to the 2019 CBO report: https://www.cbo.gov/publication/55331 . Page two shows basically the same two graphs. The only difference is that in 2023 we are further along and debt is higher than predicted in 2023.