Global Inflation to Start 2023

Inflation is the number one economic topic in nearly every country of the world. It harms lower and middle income families the most so it drives inequality. Fighting it may cause recessions and leads to higher interest rates. Higher interest rates make government spending and debt even more problematic. And so on.

So, to start the year, I thought I’ll look at inflation around the world. It also helps you put your own country’s inflation into a broader perspective. Are we alone? Are we unique? (Short answer is “no”).

The IMF World Economic Outlook Data Set[1] produces a convenient global map that I’ll use but data isn’t the freshest. Normally that’s not a problem, but with inflation changing rapidly today, it does. I update whenever I notice a serious difference between the map and the current inflation rate. The good news is that, in most cases, inflation fell a little in the last month(s) since the IMF made the map.

Also, this is a long column. I tried to make it user friendly so you can scroll, skip and look at regions of special interest to you.

Outline (in case you want to skip around)

Global Overview with a Note on North America

Europe and the War Effects

Africa

South America

Asia

Global Roundup and Conclusions

Keep in mind that dark green (5-10%) can still include relatively high inflation. It includes countries with 6% or so, like Canada, as well as countries with over 8-10% inflation, like Germany. Light green (3-5%) is better. Light and bright green (0-3%) is the target range for most countries. Only three countries on the map have that “target” inflation: China, Saudi Arabia and Japan. Japan today actually has 3.8%, so it’s not light/bright green anymore. China’s data I don’t trust. That leaves Saudi Arabia as the only country shown on the map with 0-3% inflation that still has inflation in that range (2.9% today) and has data I trust.

Inflation is indeed a world-wide struggle today for the people in essentially every country in the world.

Global Overview with a Note on North America

North America looks pretty uniform. Canada (6.8%), the US (7.1%) and Mexico (7.8%) are all in the 5-10% inflation range. That’s still above the inflation targets in those countries, but inflation over time actually have stabilized and started to decline. A few months ago, it peaked at 8.1% in Canada, 9.1% in the US, and 8.5% in Mexico. So the numbers today are actually mildly encouraging.

Inflation generally warms up as we move south across the equator. The two hot spots are Argentina (92% inflation) and Venezuela (210% inflation), both of which fell into disarray well before Covid. Chile (13.3% inflation) and Brazil (5.9% inflation), on the other hand, appear to be typical Covid cases. They both had low inflation (2-5%) for a few years, let loose during Covid and are dealing with the consequences now.

The biggest thing that otherwise jumps out from the global map is the giant pink Russia (13.8% inflation) and the very light green China (2.2%). I don’t trust the data from either of those countries.

Africa appears mixed and there’s a serious Western Europe - Central European divide. Western Europe is also pretty uniform with 7-10% inflation while Central Europe averages 17% inflation with Hungary and Lithuania suffering inflation around the 22% level today.

Europe and the War Effects

Zooming in on Europe, we can see that, indeed, inflation looks worse the closer countries are to the Russia-Ukraine war. We’d expect them to be more affected by the war and its related challenges.

Most of the people of Central Europe (in the middle of the map) suffer from inflation of 17% or so. The Ukraine itself has 20.6% inflation, but I expect wartime statistics are largely inaccurate. North of the Ukraine, we have Belarus at 13% inflation, followed by Lithuania then Latvia, both with inflation around 20-22%.

How Much Is War-Driven Inflation?

I think the initial conclusion from the map of Europe is that inflation is high, 5-10% generally. That’s due, in my opinion, to government mismanagement of fiscal spending and monetary policy. It might be lower without the war in the Ukraine, it might not.

Let’s assume that, without the war, it would look more like North American inflation which averages 7.1%. Since Europe is averaging 10.1% inflation, we might argue that the remaining 3% difference[2] might be attributable to the war. It’s just a rough guess. For Europe, then, 70% (7 of the 10%) of the blame for inflation falls on policy makers and 30% (the remaining 3%) on the war.

Central and Eastern European (CEE) inflation would probably look like Western European inflation, around 10%, but averages 17% instead. The same logic suggests that 7% inflation is the result of bad policy (like in Western Europe), 3% is the same war effect as in Western Europe and then there’s another 7% for being so close to the Ukraine, having tighter economic ties with both the Ukraine and Russia and having to struggle with more burdens of war, displaced refugees and the like.

That means the Russian war on Ukraine - based on this rough guesstimate - is accounting for almost 60% of the inflation (10%/17%) in the CEE region and the remaining 40% (7%/17%) is the result of bad policy. My honest guess is that it’s more like 50:50, but there’s no point splitting hairs.

Turkey is the big purple country below the Black Sea with 70% inflation. That’s all due to bad policy, as far as I can tell. Inflation in Turkey was 5-10% from 2014 until 2017, when Erdogan returned to power. Since 2017 it’s risen consistently, peaking at about 25% in 2018, then staying 10-20% until Covid when it ballooned to over 80%. That’s clearly bad policy[3].

Africa[4]

Nearly all the countries on the African continent have high inflation. South Africa, on the bottom, has 6-7% inflation. It’s green neighbor, Nambia, has 6-7% inflation. Both are a little high, but not too bad.

Above them are Botswana in pink (12%), Mozambique in pink (11.3%), Zimbabwe in dark purple with 244% inflation, Zambia in pink (9.9%), and Angola in red with 15%. We won’t walk through all of them, but it’s clearly mixed. There are countries in the middle with lighter green, but none in the 0-3% range. The other dark purple country is Sudan with 103% inflation.

The bright green country is Saudi Arabia, technically middle East, with 2.9% inflation. Its middle Eastern neighbors are all in the 3-10% inflation range with Yemen (bright red, below Saudi Arabia) at 43.8%.

South America

The South American countries also show a wide range of inflation rates and, sadly, policy has only worsened in that region in recent years. We’ll focus on the three largest economies – (in order of size) Brazil, Argentina and Chile - with brief comment on Venezuela.

Starting at the southern most tip of the continent, Chile in pink has 11.6% inflation[5]. Chile was traditionally an inflation targeting country and a thriving economy. It still maintains a 3% inflation target and has been raising interest rates to get inflation back under control.

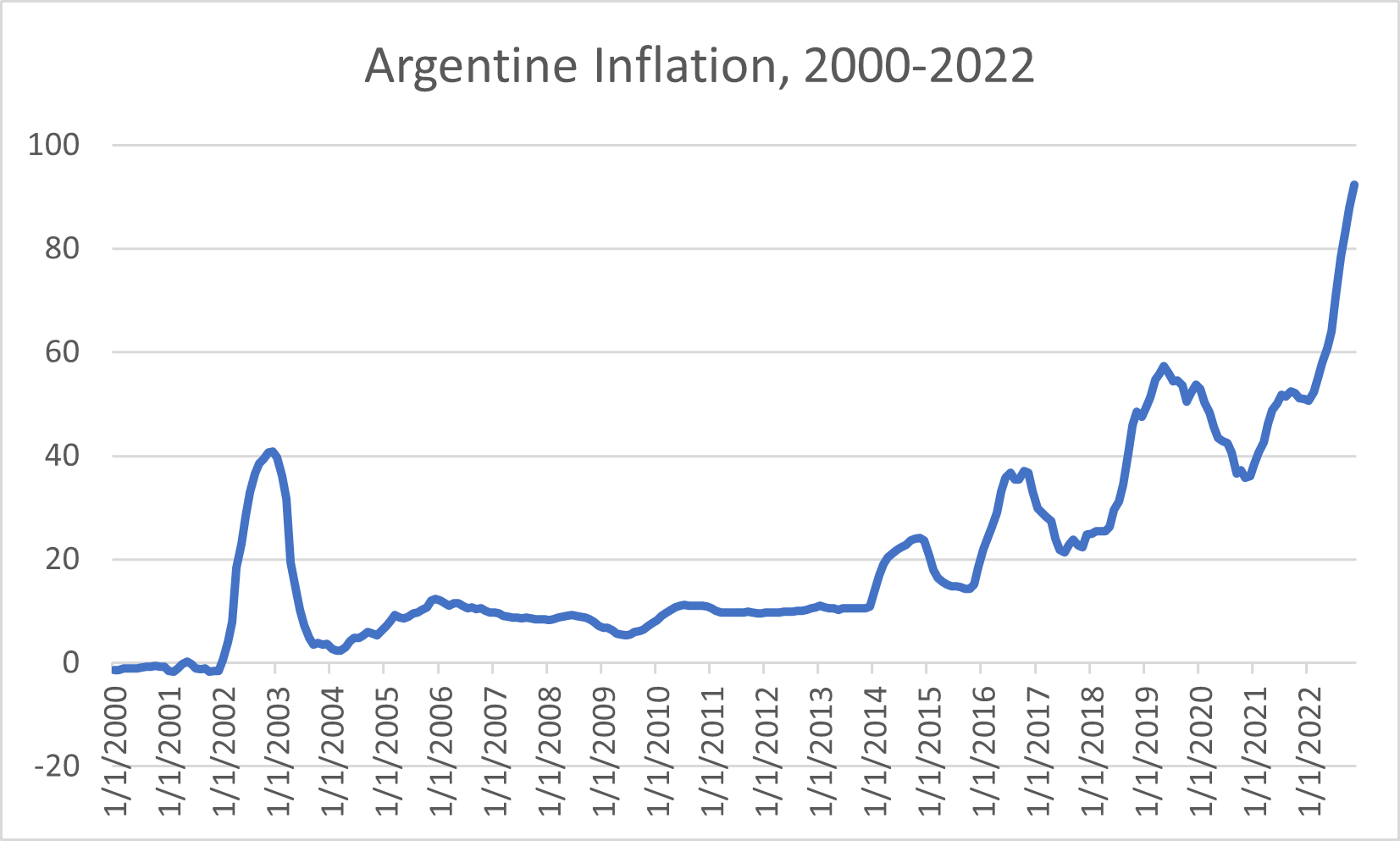

Argentina is the second largest economy in South America, after Brazil. It suffered serious hyperinflation in the 1980s with inflation hitting around 20,000% in 1990. Then in the 1990s Argentina adopted a hard currency board, fixing the peso to the US dollar, and enjoyed low inflation through most of the 1990s. Things broke down when the Russian financial collapse at the end of the 1990s led to an Argentinian crisis in 2002. Since then, Argentina has struggled.

The above graph is made from data from the Central Bank of Argentina[6]. The 2002 crisis led to money financing of debts and government spending. Inflation spiked to 40%.

From 2004 to 2014, inflation was around 10% which is high, especially after a decade of low inflation, but things clearly began spinning out of control in 2014. That cyclical pattern suggests either political cycles or efforts to control inflation, then policy makers caved when things got hard and printed money again. That is the start-stop policy trap US Fed Chair Powell and other central bankers want to avoid.

Brazil, South America’s largest economy, looks better in comparison to Chile and Argentina, with inflation at 5.9%[7]. Brazil also suffered hyperinflation in the 1980s and early- to mid-1990s, but has averaged around 6% or so ever since, peaking at 17% in 2002 with the Argentine crisis.

From 2018 Brazil enjoyed 2-5% inflation until Covid hit and monetary/fiscal policy clearly got out of control, causing inflation to spike to 12% by April this year. Rate hikes and tighter policy has brought it down since then which gives a lot of hope that Brazil will re-conquer inflation in the coming months and certainly the coming year. Let’s hope the new government keeps it on the same path.

Venezuela has been driven into the ground since Hugo Chavez took over in 1998, turning it into a socialist dictatorship. That policy has been continued by the Nicolas Maduro regime starting 2013 after the death of Chavez.

Surprisingly, Chavez got inflation under control and kept it around 10-30% a year for most of his rule. Maduro seems to have pushed the monetary gas pedal, however, as soon as he got in office. Inflation rose from 20% in 2012 to 56% in 2013 to 68% in 2014 to 180% in 2015 then hit 274% in 2016. 2016 is the last year of official data I can find. This IMF graph estimates Venezuelan inflation at 210%, but who knows. Dictatorship statistics are un-reliable.

Asia

Returning to the global map, Asia looks okay.

China in bright green shows only 2.2% inflation. Maybe that’s right, maybe not. I do not trust any Chinese statistics for the same reason I don’t trust Russian, Venezuelan and other statistics from non-transparent regimes.

India shows 5-6% inflation. I have no reason to doubt that. Thailand (5-6%), Cambodia (3-4%) and Vietnam (4-5%) are all in reasonable ranges with Myanmar at 20% and displayed in red above them.

The IMF Map shows Japan with 2% inflation, but that number is a little old now. Japan’s inflation today is around 3.8% which recently caused them to raise interest rates. This is a country to watch since that’s the first interest rate hike in many years. The Bank of Japan kept rates at near zero from about 2000 until 2016 when it lowered them to -.1%. So, their first interest rate hike in December 2022 was an historic event and everyone around the world is watching to see how the Japanese economic situation develops.

South Korea is the dark green peninsula with 5% inflation. Japan and South Korea are big economic power houses in the region and their low inflation probably helps mitigate inflation in the region overall.

Finally, a quick look south of Asia to Australia and New Zealand, also two regional economic heavyweights. They had famously hard lockdowns, but otherwise have traditionally had fairly open, vibrant economies. They are both dark green with inflation at 6-7% in Australia and 7.2% in New Zealand. Both have inflation targeting central banks and active policies to fight inflation.

Global Roundup and Conclusions

North America

Relatively speaking, North America is in okay shape. Yes, inflation is high at 6-8%, but the central banks are raising interest rates and tightening financial conditions. That should slow inflation unless the fiscal sides of government go on spending sprees. We just saw such a spending spree in the USA with an end-of-the-year spending package. So, we aren’t out of the proverbial woods yet. Nevertheless, I believe inflation will continue to fall this year, barring something truly unexpected.

Europe

Europe is just starting to take inflation seriously and has a way to go. The Russian war on Ukraine continues to put additional pressure on that region, pushing Central European inflation into very painful territory (10-20%). That will have to be addressed but will also be a major policy challenge.

The incentives are bad for policy makers. It’s hard politically to justify tightening one’s fiscal and monetary belts during a time of war, energy and humanitarian crises. Furthermore, if half the inflation is coming from the war in the Ukraine, then tightening domestic policy in, say, Hungary or Poland will probably only help with about half the inflation rate anyway. So, it will be very easy to justify spending more and only fight inflation half-heartedly. That could lead to even higher inflation.

My guess for Europe is that Western Europe will tighten and start to get inflation under control but suffer a serious recession as it does. This will ease pressure on Central European inflation but, adding recession to war will make spending and money printing very tempting. Overall, I think inflation will slow in Western Europe and remain the same or even rise in Central Europe. I very much hope that I am wrong.

South America

South America looks set to have high inflation for a while. Chile has a good chance to get inflation under control. It still has an inflation target and is raising interest rates to get there. That’s hard to do in an inflationary region when all your neighbors and trading partners are inflating, but it is possible and they still seem to have the institutions in place to achieve that.

Argentina doesn’t look set to reform any time soon. The problems started long before Covid and are deep. I don’t see much if any progress in 2023 for Argentina.

Brazil is an open case. They just had elections and a lot depends on the new government. At 5.9% inflation, a well-supported central bank can certainly get inflation back down to its 3.5% inflation target.

Asia

In terms of inflation, Asian economies overall seem to have gotten less far off course than other economies in the world and thus have a good chance to bring inflation down.

The Japanese central bank is finally raising interest rates. This is a first increase in interest rates in more than 20 years. Japan will stay in the headlines this year as it embarks on a new economic policy path.

The Bank of Korea is an inflation targeting central bank with a 2% target, up-to-date inflation reports, and has been raising its policy rate to get inflation from 5% back down to 2%. Unlike other central banks, the Korean policy rate never got trapped in near zero territory after the financial crisis. It was low, between 1.25% and 3.25% after 2008 but that’s still not as low as we saw in the US, Europe or Japan. This gives me hope that South Korea will be comfortable raising rates and tackling inflation.

Australia and New Zealand should be able to get inflation back under control. Both have the experience and the institutional commitment since both have inflation targeting regimes as well. They are raising interest rates but inflation seems to persist around the 6-7% level. I suspect they can get inflation back down, but it looks like they have a way to go still.

Africa

Based on the little information we covered in today’s column, I don’t see any main driver of inflation in that region other than Covid and bad Covid economic policy. Every country threw the monetary coffers open and inflation is now running rampant.

Like every other region, it’ll be up to each nation’s central bank to squeeze that liquidity out of the system and fight inflation. It’ll be up to each nation’s government to keep spending under control so as not to add further fuel to the inflation fire.

The South African central bank has the history, experience and institutions to lower inflation. It is also an inflation targeter with a target of keeping inflation between 3% and 6%. They claim that current inflation is 7.4%, so there is every reason to expect they can achieve 6% in 2023, the upper bound of their target range

Overall

It’ll be a tough year of inflation fighting. It’ll be a tough year politically as countries enter recessions as a result of their battle with inflation. That makes predicting policy very difficult. And there are outside factors like the Russian war on Ukraine that are truly outside the scope of policy predictions.

But I think we’ll see progress on the inflation front. No one in the world thinks it’s transitory any more. No one thinks its just supply chain problems. And no one thinks its just the Russian war on Ukraine.

Clearly a lot of it was the result of bad policy around Covd. Fortunately, we are further and further away from those core Covid years now and the effects of bad policy should fade by the day.

All this means that there will be a lot of unpredictable financial movements in the coming year for sure. With every country raising interest rates while inflation continues to rise in some places and falls in others, currencies will move all over the place relative to each other.

And exchange rates and interest rates drive international financial investment flows from one country to another. So those will shift dramatically and haphazardly this year as well.

I guess one thing is clear. I should have plenty to write about in 2023.

Thanks for reading.

[1] IMF World Economic Outlook data and graphics: https://www.imf.org/external/datamapper/PCPIPCH@WEO/OEMDC/ADVEC/WEOWORLD?year=2022. Also note that the IMF creates its maps with a big of a lag, so the inflation rates are a little different than if we look at the numbers today.

[2] European average inflation minus North American average inflation, 10.1% - 7.1% = 3%.

[3] In all fairness to Mr. Erdogan, during his first time in office (2003-2014) inflation was 5-10%.

[4] I updated the inflation numbers in this section with the latest data from Trading Economics (https://tradingeconomics.com/countries) since the IMF map seemed to be farther off here.

[5] The Chilean central bank reports 13.3% inflation, so this IMF number is a little old: https://www.bcentral.cl/en/areas/monetary-policy

[6] Argentine inflation data. https://www.bcra.gob.ar/PublicacionesEstadisticas/Principales_variables_datos_i.asp . You can go there yourself and set the dates from 1980 to 1995 and see the 20,000 percent inflation by 1990 if you like.

[7] From Trading Economics: https://tradingeconomics.com/brazil/indicators