Interest Rates, Interest Rates Everywhere

After keeping interest rates low for years, central banks around the world are raising their policy rates to fight inflation. This is just the beginning.

Interest Rates, Financial Capital Flows and Exchange Rates

In an open world where money can move anywhere in search of the highest return, one effect of raising interest rates is to attract international financial capital into your country and raise the value of your currency.

The mechanism works like this: your country’s interest rate rises which means investors can move money out of other countries and into investments in your country that pay this higher interest rate (i.e., return). To invest though they need to buy your domestic currency so they can put that money into your economy in banks, stocks, etc. When they sell their own currency to buy your country’s currency, this increases demand for your country’s currency, pushing up its value.

The US dollar’s value has been rising relative to most other currencies for most of this year. This is partially because the US is a safe haven country – that is, it’s viewed as a safe place economically relative to other countries – and also because the US economy looked strong coming out of Covid, so money flowed in to invest in good growth opportunities.

This FRED graph captures the “Value of the US Dollar” relative to other major currencies. It clearly fell in value during Covid, 2020-2021 and has been rising since mid 2021 and all 2022 so far.

When Covid broke out, there was a quick flight to quality that pushed the USD’s value way up (see the spike in the grey Covid recession section on the graph). But after that the USD lost value. It wasn’t clear the US was doing better than other economies. As we all recall, every few weeks there was a new “example country” for everyone to follow in terms of how well it was handling the pandemic. First the Swedes, then no it’s Singapore, then no it’s Europe, then Australia, and so on. In hindsight, we were all a mess and did the best we could but that’s a story for another time.

It's hard to discern completely why the USD rose in value in late 2021. Perhaps investors saw there would be US GDP growth relative to the rest of the world. Perhaps they already sensed inflation and that the US Fed would raise rates. It’s hard to know.

In 2022, the USD strengthened a lot. This is surely due to three factors: 1) the relative strength of the US economy and its positive expected growth path, 2) the war in Ukraine strengthening the US’s “safe harbor” position in the world and 3) the US Fed’s increasing commitment to raising interest rates. The Fed started off behind the ball and weak but strengthened its resolve with each passing month.

If the US were the only country raising interest rates, then it would be very clear. Every time the US Fed is believe to raise interest rates and every time it actually does raise interest rates, then the US dollar would strengthen relative to other currencies. The complication is that things never happen in a vacuum.

Who Is Raising Rates Now?

Let’s start by looking at inflation in a few key places: Canada, the UK, Europe and Japan. These are loosely considered “the Advanced Economies”[1]. In the USA, inflation is now running at 8.6%.

· Canadian inflation is 7.7%

· United Kingdom’ inflation is 9.1%

· European Union’s inflation is 8.1%

· Japanese inflation is 2.5%

We’ll look at these in reverse order.

JAPAN. No one is quite sure why inflation has not hit Japan. Their economy is still in pretty bad shape with economic growth at zero to negative. But whatever the reason, Japan isn’t facing an inflation problem and unsurprisingly is also not raising interest rates. The Bank of Japan has kept its policy rate at -0.1% since 2016!

EUROPEAN UNION. The European Central Bank should have been raising rates. It has not and it has been widely criticized for not doing so. The European Central Bank announced in mid-June that it will cease its bond purchasing programs – at least partially – starting in July and also that it plans to raise interest rates 0.25%. Normally such an announcement would lead to a slight strengthening in the Euro’s value relative to other currencies, but it happened in a month when other countries were raising their rates and any effect was heavily diluted.

I don’t have a strong prediction for what the Europeans will do, but they are in a bad bind right now. On the one hand inflation is getting worse while, on the other hand, a lot of the price pressure is coming from energy prices given the war with Russia. And that is threatening to really harm the European economy. Raising interest rates won’t fight inflation coming from energy prices but it will slow growth. That means they get all the pain of raising rates without all the benefit.

The problem is that inflation is 8.1% and much of that is still due to central bank mismanaging money in the European Union. Their official inflation target is 2% over the medium term. If they do nothing to fight inflation, they lose all credibility. And if even half of that 8% is their doing, then they are the only ones who can undo it. So, they must act and in today’s world, “acting” means raising rates to fight inflation.

The European Central Bank has announced that it will cease bond purchases and raise rates consistently from here on out. It will also continue to make announcements about future rate hikes well in advance. But it will be challenging and I certainly don’t envy the leadership there. Very tough.

UNITED KINGDOM. The UK is facing the highest inflation of the group today at 9.1%. They announced that they expect it to continue to rise and possibly peak at 11%. Wow! 11% just doesn’t seem real in the modern UK economy.

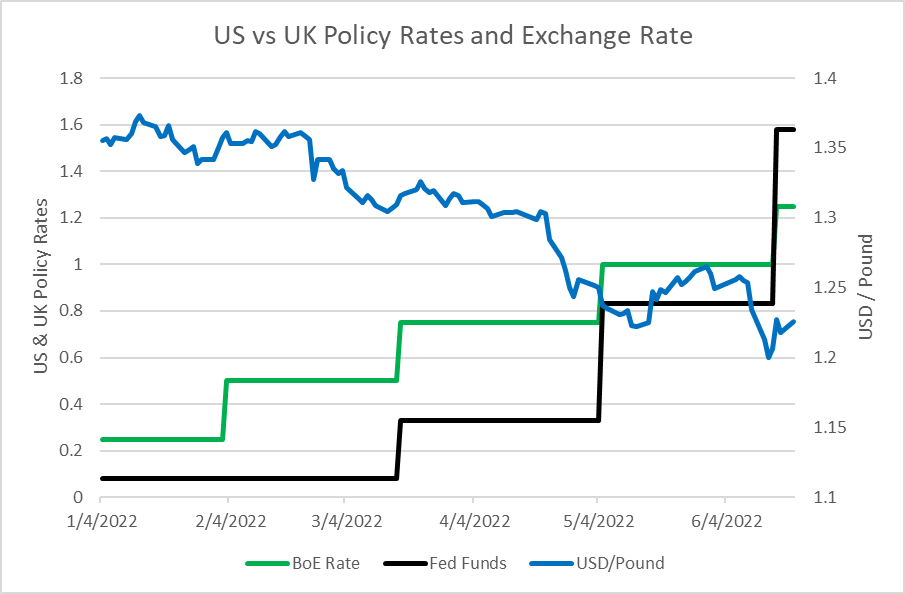

Interestingly though, their rate hikes don’t seem to have been sufficient to strengthen the British pound relative to the USD. The graph below shows the UK’s Bank of England rate (BoE Rate), the Federal funds rate (Fed Funds) and the USD to Pound exchange rate.

It’s important to stop and think for a second about the exchange rate. With USD/Pounds, when this goes up it means people must pay more and more USD to buy 1 Pound so the USD is becoming weaker or less valuable (relative to the Pound). When this falls, people pay less USD for 1 Pound which means the USD is stronger or more valuable (relative to the Pound).

The USD stayed pretty flat relative to the Pound through the UK’s first rate hike in February. The USD has been gaining strength ever since however. The decline starting around 3/4/2022 likely occurred in anticipation of the US Fed finally raising rates, which it did. But, interestingly, the Bank of England has been raising rates at the same time as the US Fed. This is to fight its own inflation challenges but also likely timed to prevent large currency swings. Central banks will often discuss and coordinate policy moves even though they primarily consider domestic issues when setting their rates.

The USD however continued to strengthen thereafter and it will be interesting to see where it goes from here after the recent .75 basis point Fed funds increase. Since the UK has kept with .5 point increases and the US is clearly starting to increase more strongly, my guess is that we’ll continue to see the USD strengthen relative to the Pound for some time.

Overall though, it’s pretty clear that the US rate hikes are the dominant effect in defining the USD to Pound relationship.

CANADA. The Bank of Canada also began raising rates before the US Fed did. And the effect seems to have been to strengthen the Canadian Dollar relative to the USD. Again, the blue line (right axis) is the USD to CAD so an increase is a weaker USD and a decrease is a stronger USD.

The initial strengthening of the CAD (weakening of the USD) is seen in that 3/4/2022 to 4/4/2022 period. One could argue that it’s a response to an unimpressive quarter point move by the US Fed, perhaps revealing a lack of seriousness about inflation. I’m cautious with such statements since, again, a lot is happening in the world.

But the USD clearly weakened after the first Fed funds increase and then strengthened a lot going into the next rate increase. For sure, every observer could see the Fed was getting more serious by this point, reducing bond purchases as well and openly admitting inflation was a problem.

The Bank of Canada’s half point increase on 4/13/2022 strengthened the CAD (weakened the USD) for a moment, but it looks like markets anticipated the US Fed’s 5/5/2022 half point hike as it also became increasingly clear that the Fed was going to continue to raise rates through the year.

The weakening of the USD thereafter is a mystery. Was it anticipation of the Canadian rate hike? Were other factors at play? It’s hard to say.

Again, with the last Fed rate hike, however the pattern is clear and the USD gained strength once again.

Interpreting Both Cases

Markets are hard to read. As an economist, I aim to explain markets and understand their functioning. I don’t try to time and predict in an effort to turn a profit. I leave that for my friends in trading.

But it’s pretty clear that in the case of the USD versus Canadian dollar that money flows look like they are much more responsive and seem to be more forward looking than they are between the UK and the US. The US and Canadian economies are both large and important in global markets. It makes sense their policy moves would have large effects on their currencies. And, if the interest rate changes are important, then it makes sense that investors would spend time and energy anticipating changes rather than just responding after the fact.

The UK to US story is different and sadly suggests the UK’s role in world financial markets has indeed diminished some. One result of Brexit – Britain’s exit from the European Union – is that financial centers left London. Perhaps that has already had a negative effect on the relative importance of UK monetary policy on world markets. While the US and Canada seem to be balanced, both moving the exchange rate, the US seems to totally dominate in determining the USD’s value relative to the British Pound.

Everyone Moving At Once

To close, we’ll look at all the policy rates together. I left Japan and the EU out since neither has done anything yet. But you can see the trend. Rates are rising and the steps are getting bigger. I wouldn’t be surprised to see a larger step for the Bank of England rate in the future if inflation keeps rising.

I was caught off guard by the Fed’s .75 point increase. While I argued from the beginning that rates will need to rise a lot, I wasn’t sure when the Fed would finally get on board and start doing it. It seems that now is when they are finally waking up to reality.

Nevertheless, I still anticipate that the coming 3-4 weeks will be key. We’ll see the Q2 GDP numbers for the US and get more inflation numbers. I am expecting them to look a little worse than everyone has been anticipating. We’ll be back to the drum beat of “the recession is here, the recession is here”.

Soon the Europeans will start raising rates as well. Predicting exchange rate movements will become increasingly difficult the more banks there are raising rates. But the fundamental trends are the same. All else equal, as one country raises its rates, it will strengthen its own currency relative to others. If two countries raise rates at the same time, the bigger country will have a stronger effect, and when equally weighted the timing and anticipation will matter a lot.

[1] Of course others like South Korea, Australia and New Zealand, to name a few, would fit into this category as well, but in the interest of space I focused on our major trading partners.