King Dollar Worries: Much Ado About Nothing

Photo by Kenny Eliason on Unsplash

Every few years alarm bells go off and headlines report the decline of King Dollar. The USD is losing its position as the world’s reserve currency! The sky is falling!

This has recently become a hot topic again. I’m not entirely sure what exactly inspired it this time, but figured I’ll address it anyway.

How the USD Became the World’s Reserve Currency

The USD wasn’t always the world’s reserve currency. And there’s no reason that it must be the world’s reserve currency.

Coming out of WWII, the US and other developed economies established a new global monetary regime intended to provide economic stability, promote trade and prevent future wars. World leaders met at a conference in Bretton Woods, New Hampshire, and the resulting agreement came to be known as “Bretton Woods”.

The idea was simple. The US monetary authorities would peg the value of the USD to gold. Then, all other countries would peg the values of their currencies to the USD. While this meant all major currencies were ultimately pegged to gold (through the USD), it also placed the USD at the center of all global finance.

Bretton Woods was a transitionary regime in the grand scheme of things. It built on gold which connected it to the “old world” when nearly every country tied their currency to gold. But it also transitioned to a new world order of financial coordination via a system of fixing currency values to the USD. In the same way that countries had naturally built up stocks of gold in the old gold-backed-currency regimes, this new regime required every country to build up stocks of USD instead.

An aside on fixing prices and stocks of things.

As I explained last year in The Problem with Price Controls (July 2022), when you fix a market price, quantities must do all the adjusting in a market. Fixed exchange rate regimes are a perfect example of this. In a global market, one country can’t just pass a law that the price of something that’s internationally traded is going to be X.

Imagine someone announcing they want to fix the price of apples at $1.00 per apple (and assume for a moment that all apples are the same). They could do this, but they’d have to have a giant stock of apples to make it work. If they had enough apples, and could transport them fast enough and at super low cost, then either everyone would buy from them if other sellers were more expensive or sell to them if other buyers were not willing to pay as much. The result would indeed be a fixed price of apples since no one would be willing to buy for more or sell for less than $1.00.

The same is true of a currency. When a country fixes, or pegs, the value of its currency to the USD, it must first build up a stock of USD called “international reserves” so they can always buy and sell their own currency in world markets. That’s why the countries with currencies pegged to gold had stocks of gold and those pegging to the USD had (and still have) stocks of USD under Bretton Woods. (Note that they don’t need a stock of their own currency too since they are the ones who print their own currency so they have an infinite supply available at any time.)

This new regime with the USD as the central linchpin also occurred when historically trade and economic growth exploded around the world. The following graph from the World Bank (which I used in my December 2022 column) reminds us of that global growth period, post-WWII.

And this means that, by chance, the period when everyone agreed to set the USD at the center of all global finance and commerce was also the period when the world saw the most economic growth ever.

Oil markets grew during this period along with a boom in automotive sales. Oil-rich nations rose in power both economically and politically. And, naturally, oil and other major commodity contracts were done in USD. This just entrenched the role of the USD in every aspect of global economic life.

For those of you interested in the role of the USD in world oil markets and financial markets, listen to this great Odd Lots Podcast on the origins of Petro Dollars and Euro Dollars (it’s a bit nerdy…but great!): https://omny.fm/shows/odd-lots/josh-younger-on-the-surprising-origins-of-eurodoll

So, the new Bretton Woods system fixed currency values to the USD. This required all participating countries to have stocks of USD. And, the USD was also playing this new, central role, right when the world economy blew up – in a good way – and therefore it made sense to base new trade agreement in USD as well.

This whole nexus of global financial arrangements, all being based in US dollars, is what is meant when people say the USD is “the world’s reserve currency”[1].

Beyond the economic reasons, of course, the USA also became a super power at this time and then, with the collapse of the Soviet Union, the USA became the sole super power. One more thread weaving the fabric supporting the role of the USD as the central global financial currency.

Post-Bretton Woods (1971) to the Birth of the Euro (1999)

The Bretton Woods system collapsed in 1971 when the US decided to exit and then let the USD freely float in world markets. We forget today how controversial that was.

To the best of my knowledge, that was the first time in history that a country intentionally moved to a fiat currency system as the permanent monetary system. For the first time in US history, the currency was intentionally not connected to either gold, silver or other commodities nor to the value of another currency. It was based 100% on the value of and faith in the US government.

If anyone knows of historical exceptions, even back thousands of years, message or email me, I’d love to find some of those exceptional cases where, intentionally as a matter of sustained policy (i.e., not just temporarily during a crisis or war), a country’s currency wasn’t either tied to the value of gold, silver or other commodity or another country’s currency.

When the system collapsed, the USD floated freely. The Europeans – the other major partners in the arrangement – tried to maintain a fixed exchange rate system amongst themselves that continued to stumble along, in and out of crisis, until 1999 when they all adopted the Euro and eliminated their own, domestic currencies completely.

In the meantime, following WWII, Japan rose as a dominant economy as well. As a natural result, countries primarily trading with Japan wrote contracts in Japanese yen, held more yen in their reserves and so on. Japan grew so large that it became the second largest economy in the world, after the USA, by the 1980’s.

After the birth of the Euro, the European Union[2] - a collection of large national economies - became the second largest “economy” after the US. Many countries around its periphery pegged their currencies to the Euro as more trade relations started to be denominated in Euros as well.

If you measured reserves around the world in 1972, right after the end of Bretton Woods, you would have found the USD was by far the dominant reserve currency. My guess is that 80-90% of central bank reserves would have been USD. The rise of Japan meant that the percentage would have been lower in Asian countries. Japan’s rise would also naturally mean some decline in the USD’s share in world reserves everywhere over time. Then, add the birth of the Euro (1999) and, sure enough, the USD’s share declined naturally.

All these factors have lowered the USD’s share in global reserves over the years.

Other Sidenotes: England and China

Two other factors have led to major changes in the composition of currencies for trade and that were held in reserves. The first is the expansion of the United States’ role and global influence and the decline of the British Empire’s size and scope. And, the second, is the rise of China.

I already explained the rise of the US, but it’s important to note that the rise of the US took place alongside a decline of the British Empire. The British pound sterling was also a historically important currency and, in many ways, was “the world’s reserve currency” before the USD.

The British Empire touched most of the world for a very long time and still has a connection in India, Australia and Canada, just to name a few and remind us of the persistent scope of its influence. As the British Empire shrank, the United States grew, in terms of global influence on trade and finance. This contributed as well to the rise of the USD as the reserve currency and the decline of the pound sterling.

While this UK to US switch was playing out early last century, the beginning of this century was dominated by the rise of China. China’s is the second largest economy today, after the US. Third is the European Union as a whole. Or, if you count countries, then Japan is 3rd, then probably Germany. Otherwise, most people count the US, China, EU, and Japan as the top four, in that order.

However you measure it, China is number two. It stands to reason that the Chinese renminbi would grow in importance as a currency and hence start to be held as a reserve currency, further lowering the USD’s share.

Where Are We Today

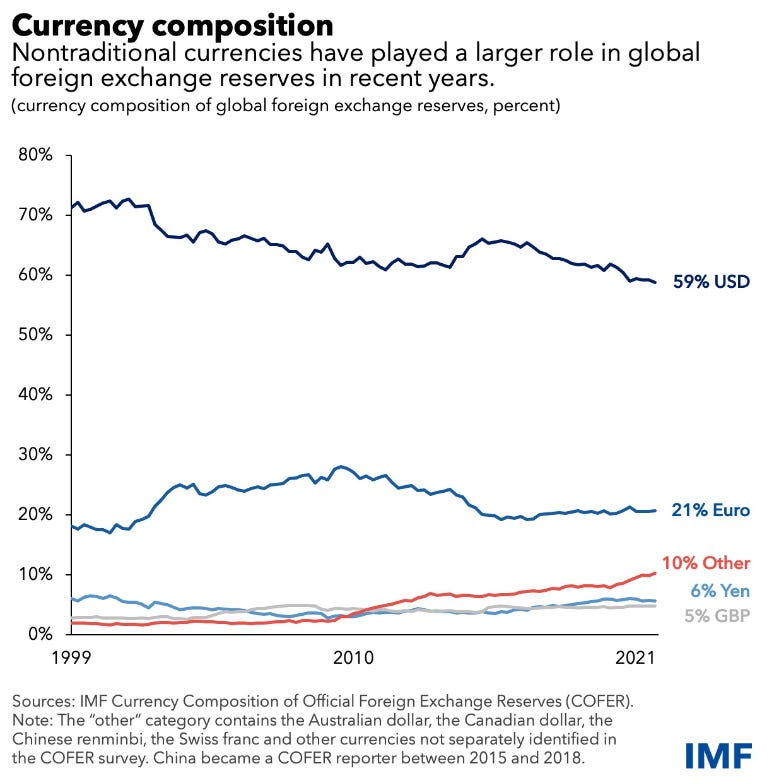

Serkan Arslanalp, Barry Eichengreen , and Chima Simpson-Bell have an excellent piece at the IMF on “Dollar Dominance and the Rise of Nontraditional Reserve Currencies”[3]. Their graph below illustrates where we are today and how it has evolved over the last 20 years or so.

The graph shows that in 1999 the USD’s share of currencies in reserves around the world was about 72% and today it’s about 59%. At the start of the graph, in 1999, the 18% or so assigned to “Euro” was likely made up of other national currencies (German Deutsch mark, French Franc, etc.) that all were then combined into the single Euro. That is to say, the share of the collection of all the European currencies was likely about 18%. Consolidating into one currency clearly added to its popularity as a reserve currency as can be seen in its rise over the coming 5 years or so.

It looks like it took a few years for the Euro to establish itself, peaking at almost 30%. It looks like the rise of the Euro took shares from both the USD and the Japanese yen both. The British pound (GBP in the graph) also gained a bit during that period. That makes sense because Britain was part of the European market, although not sharing the currency. But it meant that, as the market grew, so did likely usage of the GBP.

That 2000-2010 period is when I first started seeing regular articles asking about the future of the USD as the world’s reserve currency and whether the Euro would replace it. One can see why with the sudden rise in the Euro and decline in USD percent. Again, the graph suggests that the situation of the USD indeed ceased to “worsen” likely explaining why interest in the topic also faded from the headlines..

You can see in the authors’ note below the graph that the “other” category contains the Chinese currency as well as the Australian dollar, Canadian dollar and Swiss franc among others. Other currencies have been growing in prominence, but they are not the major threat to the USD’s continued dominance. If anything, “other” is a surprisingly small category given the size of the Chinese economy. This means that, despite the Chinese economy’s size, the Chinese renminbi isn’t even 10% of reserves around the world.

The authors note elsewhere that they see market forces playing the largest role, not politics, in determining the shares. They identify three key drivers (read their article for details): 1) “growing liquidity of markets”, 2) “central bank reserve managers have become more active in chasing returns” and 3) “as yields on bonds issued by the governments of the Big Four countries have fallen toward zero, central bank reserve managers may have intensified their search for higher yielding alternatives”.

Drivers two and three will decline as world interest rates rise and stay high for the coming years. It’ll be interesting to see the shares in, say, 5 years.

What’s the Benefit of Having the World’s Reserve Currency?

One question remains in the back of my brain through all of this: who cares? US news outlets and politicians - or at least political commentators on occasion - make a big deal about the USD being the world’s reserve currency. But, then again, they love to cast market interactions and shifts in trade as conspiracies and global political struggles. I and most economists view markets as allowing mutually beneficial cooperation.

Nevertheless, it is quite legitimate to ask what the benefit is of having a world reserve currency.

The main benefit, to be honest, is that trade with the US is a bit easier because the transaction costs of dealing in USD are lower because everyone uses and has access to your currency. Secondarily, there are some potential benefits in having lots of trade denominated in USD. It means that the US is less likely to be influenced by foreign inflation but other countries are more likely to catch our “inflation illnesses”. In global economics, it’s often said that when the US gets sick, the rest of the world catches a cold. It sounds cruel, but if you have to choose which side of that relationship to be on, it’s better not to be the one catching everyone else’s colds.

Third, the US government likes to have the world’s reserve currency because it means there is always a natural and deep market for US government debt. Every country’s central bank, global private banks and so on all demand US Treasuries as highly-liquid alternatives to holding pure cash. For banking purposes, they are often considered money – in some ways more so – than cash itself.

Usually when people discuss “the benefits” they actually mean the last one. It’s helpful to the US government to have access to natural and persistent demand for its debt. But I don’t know how good that is. Do we Americans really want to make it easier for, to encourage and incentivize, our government to run bigger deficits and borrow more? I don’t.

By making debt issuance less costly, it encourages the US government to borrow money and that leads to other problems. Additionally, it means that, if the US ever truly has financial problems, they will spread immediately to every corner of the earth and cause a global economic earthquake that we actually haven’t ever really observed historically. It would be bad, but we almost can’t imagine exactly how bad and in what ways. This makes the global financial system fragile in a very strange sense.

We saw hints of that with the 2008/09 Global Financial Crisis. A true US budget crisis and real potential default on US Treasuries would likely be much worse.

The fourth benefit, in my mind - although again one the pundits put high on the list - is the political benefit which is also tremendous for those in power in the US. It means the US government can impose sanctions on other countries – witness our latest sanctions on Russia – because so many world transactions occur in USD and clear through payment systems the US either controls or can access. But that too is a double-edged sword. That means every rogue nation wants an alternative payments system and any use of USD will then be seen as a political signal.

So, yes, the US benefits. By that, economists mean it facilitates trade and that’s a good thing. Cooperation and exchange – aka “trade” – is, by definition, mutually beneficial. Both sides benefit. Trade is not a zero-sum game.

Politicians mean that having the world’s reserve currency means more global political power for the US. That political side – as is usually the case – is where all the tension lies. Political power is a zero-sum game.

Conclusions?

I think the USD’s share will continue to decline naturally as the rest of the world grows and develops economically. I’m strongly in favor of letting that happen naturally as other countries rise in economic prominence. I do not think the US government should get involved just to offset the slow decline in USDs as a percent of global reserves.

I would love to see a world where everyone “suffers” from the same first world problems we have in the US. I’d rather people everywhere worry about obesity than starvation, the cost of health care instead of its absence, and so on.

As long as the US maintains an economy that is more free market than command-driven, it will continue to grow and it’s citizens will flourish. To the extent it does, it will naturally keep a very dominant position as a global reserve currency.

I hope to see a world where other countries move in the same direction and thereby grow to a point of competing with the US in terms of largest economy. Every country that moves from command, control and authoritarianism has advanced in those areas by leaps and bounds. Witness post-WWII Japan, Germany, Chile, Brazil, Hong Kong, Singapore, South Korea, and many others and, of course, China.

But as countries have deviated from it, that growth and improvement in human flourishing has slowed or stopped. Hong Kong after returning to China is an extreme example. South versus North Korea are other examples.

China has also recently turned backwards and I predict they will therefore slow economically and, more importantly, suffer a decline in terms of human freedom. But the political power of having a dominant world currency still remains appealing to governments like China’s. It will surely continue to work with Russia and other rogue countries to develop alternative payment systems, trap countries through debt into using the renminbi and so on.

But I don’t predict China will come to dominate as the world’s reserve currency. Maybe, just maybe, with all their scheming, they could eventually get the “other” category up to 20%. But I seriously doubt they can get it higher and the gain won’t all come at the USD’s expense.

As far as I can see, given the current state of the world, the USD will remain the world’s reserve currency for the foreseeable future. I for one do not lose any sleep over it at all.

[1] Technically, “reserve currency” just means that it’s held in reserves at central banks. But in this regard many countries are “a” reserve currency.

[2] For my technical readers, yes, I’m being sloppy in Eurozone vs European Union, etc.

[3] https://www.imf.org/en/Blogs/Articles/2022/06/01/blog-dollar-dominance-and-the-rise-of-nontraditional-reserve-currencies