The Employment Enigma and the US Economy, Part One: Labor Force Participation

This is Part One of a two part series on employment and the US economy. This first part deals with labor force participation rates. The second part with unemployment.

The latest US jobs report[1] came out Friday, August 5th, and it was a shocker. The initial shock is because it shows unemployment FELL last month and employment grew by about double what was expected!

The secondary shockwave comes from the policy implications. In short, with unemployment falling, everyone now expects the Fed to double down on raising interest rates. If it had been a weaker report – a slow cooling of the labor market – like many were hoping, then the Fed might ease a little. Now, that is clearly not going to happen.

We’ll try to understand the numbers and the mystery first.

Labor Force Participation

Let’s start with a brief refresher about how labor numbers are calculated.

Conceptually, imagine an economy with 100 people in it.

Imagine that 20 of those people are not working and not trying to work. Those could be children, students, retired people, or people taking time off between jobs. They could also be people who were trying to work, never found a job and finally just gave up looking. All the people in this group of 20 are called “not in the labor force”.

The remaining 80 people are, by default, called “in the labor force” or, simply, “the labor force”. We don’t yet know if they have jobs or not. We’ll get to that in a minute. But we can already calculate a first number that is relevant today: the labor force participation rate.

The labor force participation rate is the number of people “in the labor force” (i.e., participating) divided by the total population. Here, 80/100 = .8. Or, 80% of the population is participating in the labor force.

I used simple numbers for illustration. The actual US numbers from the latest report are that the US population is about 332 million people and labor force participation rate of 62%. That means there are about 206 million people in the labor force and 125 not in labor force.

The Missing Worker Mystery

One thing that still remains a bit of a mystery is that pre-Covid, the labor force participation rate was 63.4%. If we had that today, we’d have about 210 million people in the labor force instead of just 206 million which means there are still about 4 million people “missing” in the US economy.

Just to be clear, that 63% is consistent with the long run trend of the labor force participation rate. Any “return to normal” should be back close to that. See the FRED diagram below.

You can see it’s ratcheting back up post-Covid. That’s a good thing for sure. But, it’s moving more slowly than we expected and no one is entirely sure why.

Do people have a bunch of Covid funds they are living on and therefore are loathe to return to work? We thought that might be it initially, but they seem to have spent most of that by now. See the FRED diagram for US Personal Saving.

Clearly there was a massive jump in savings during Covid. That was the result of all the direct transfers from the government combined with the fact that, initially, people all still had their jobs and income but they stopped spending at stores, restaurants, gas, etc.

The relevant part here is that it has returned to pre-Covid levels. So that’s not driving people to stay out of the work force today.

Did they retire? Some people retired early for sure. So that’s some people, but not all of the 4 million. Let’s say 1 million, just to be conservative. What about the other 3 million?

Maybe they died from Covid?!

The latest numbers I can find[2] indicate that about 1 million people in the US died from Covid. Even if we consider that to account for 1 million of those people leaving the labor force, we still have to explain the remaining 2 million.

And, not to be too impolite, but… a very large percent of those who died from Covid were older people and many were already ill. I don’t want to debate Covid here. I am far from an expert on medical matters at all. But, from an economic standpoint, the death of anyone already not in the labor force – already retired, for example – wouldn’t add to the number of people out of the labor force. It would reduce it! It would increase the percentage of the total population in the labor force.

I don’t think Covid deaths are driving this phenomenon of the missing people.

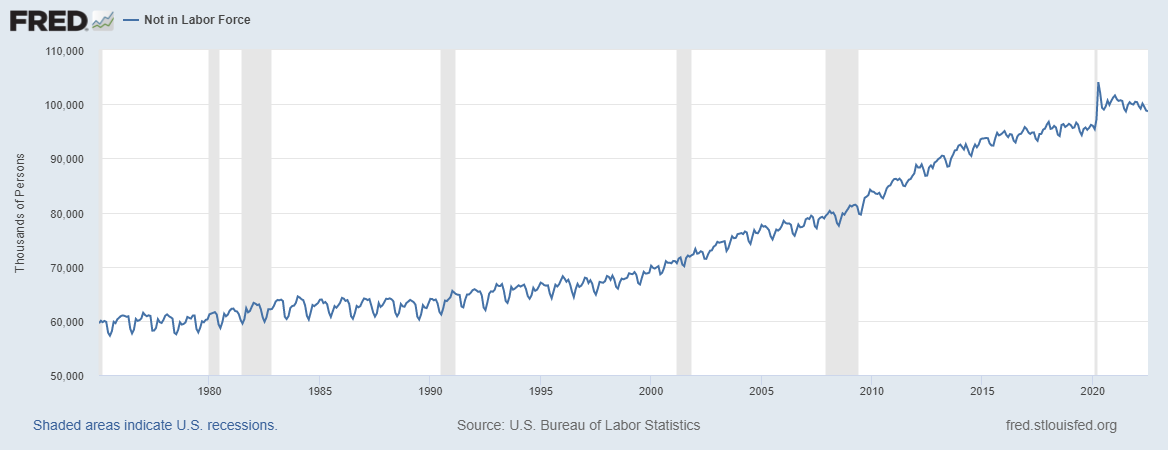

Not In the Labor Force and Trends

Here’s what the US “Not in the Labor Force” looks like over time.

I added the longer time horizon so you can see that it had indeed already been rising since the end of the 1990s. That is the baby boomer generation retiring and other broader cultural changes. And it has been a trend.

Also notice that it has a consistent cycle to it. In particular, it dips down over and over. Those are summers. The bottoms of those dips basically occur every year in July. This should give us a slight warning about reading too much into this year’s strong JULY jobs report. Now, all the analysts know this and take it into consideration, but I just wanted to point it out.

The important piece for this discussion is again that it clearly jumps up during Covid – no surprise – but doesn’t return to trend. Or did it?

One possible interpretation is to say, “look… since about 2010, the trend is clear”. In that case, there’s no surprise. See this FRED diagram.

If you add a crude trend line from 2010, actually we are right on trend and we shouldn’t expect those people to come back.

All these things are the mysteries policymakers are struggling with. I do not have the answer. It seems to me still a bit mysterious. I will admit that more of it looks like trend than I originally thought.

But I have two problems with that. First, there are two big breaks in this data if you look at it annually. The first break is around 2016. I don’t know why, actually. The second break is around 2020. That’s clearly Covid. See this FRED graph.

If you account for those breaks, it looks like there was an upward trend (red line in graph) but then it levelled off around 2016 (green line) until Covid. In this case, we aren’t on trend. We are still way off and haven’t adjusted back to “normal” (i.e., pre-Covid) levels.

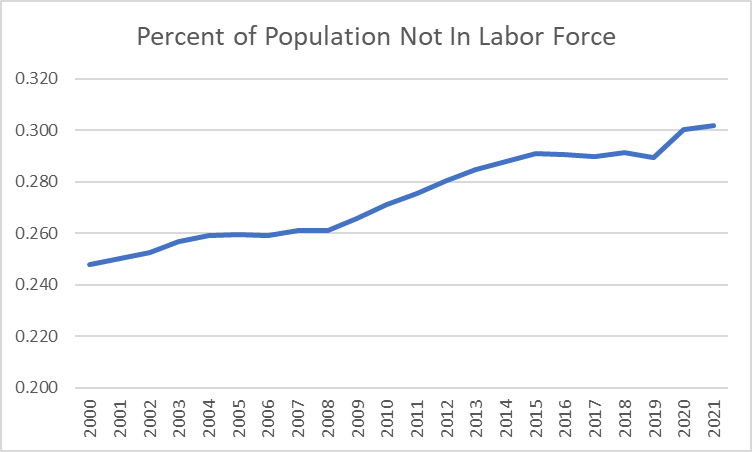

One issue is that these graphs are in the total number of people. If you think about it, the total number of people “not in the labor force” will always grow in a growing population. Suppose 30% are always not in the labor force. Then 30% of a growing population will always be more and more total people.

FRED doesn’t calculate the percentage of people not in the labor force. So, I took FRED’s “Not in Labor Force” number and divided by FRED’s Population number to get a basic, first-pass, number for the percentage of the population not in the labor force. It has also been increasing recently, then flattened a bit (around 2014).

A moment’s reflection will tell you that the percentage of people not working cannot increase forever. It can’t go to 100% for example since that would mean no one is working. It could, however, settle around 30%. Who knows?

Laws, regulations, labor restrictions, good/bad economic growth, tax policy, general cultural attitudes all influence people’s choices to enter the labor force or not.

Anecdotally, I can tell you that more and more of my students in recent years – even pre-Covid – were less and less eager to work. An increasing percentage of them would tell me they were happy to stay unemployed or work part time just to pay rent because they didn’t feel like they needed more in life. So, there is some generational change happening and perhaps it sped up during Covid.

Conclusion for Part One

What’s the point of all this?

Partially I just wanted to dig into the numbers and understand them. There are a lot of legitimate questions out there and a lot to think about and discuss. The truth is that the numbers today are confusing.

It is hard to know if we are on some long-term trend and just didn’t notice it during our two-year Covid break. If so, then we are entering a world of low unemployment for a long time because more people exiting the labor force means less people working. I’ll address that more in Part Two of this series.

That also means, however that the low unemployment rate today isn’t a policy success. It’s just part of the long-term trend. And policymakers shouldn’t be concerned with affecting it with things like interest rates today. Perhaps Congress could consider longer-term changes in tax code or regulations, but there’s little we can do now that would affect it much today.

One implication for Fed policymakers would be that they could continue increasing interest rates without worry. It may cause a little pain, but the economy is strong and can handle it. Just look at the low unemployment numbers!

But… let’s be a little more cautious. If the two-trend picture is more right, then the unemployment numbers are artificially low. Unemployment isn’t capturing all the pain in the labor market because the truly harmed have just left the labor force altogether.

In that case, the Fed should not consider that unemployment today is low and the economy strong. Instead, the economy still hasn’t strengthened enough to attract all the people back into the labor market.

The implication in that case is that the Fed should then worry about raising interest rates too fast. The economy is weaker than it appears – in terms of employment – and hence more fragile.

I’m more in the second camp. I think the employment situation is a bit weaker than it appears and it’s one reason I’ve been arguing that the broader pain is about to start now. I think unemployment will rise soon.

[1] “US Jobs Report” is actually the US Bureau of Labor Statics Employment Situation report: https://www.bls.gov/news.release/empsit.nr0.htm .

[2] I checked a few sites: https://www.worldometers.info/coronavirus/country/us/ and Johns Hopkins: https://coronavirus.jhu.edu/us-map