What The FED Will Do and What It Will Mean

Coming Up This Week on Global Economics

Online post – Global Econ Q&A: Which Interest Rates?

Late week email and post – FED Meeting Follow Up

What The FED Will Do and What It Will Mean

The Federal Reserve’s Federal Open Market Committee (FOMC) will meet Tuesday and Wednesday this week to decide its next policy steps. With inflation and recessions on everyone’s minds, the FOMC will be sure to make headlines no matter what it does.

The two most discussed decisions the FOMC makes are what it does with the key FED policy rate, the federal funds rate, and what it does with its bond purchase program (sometimes called “unwinding its balance sheet” or “quantitative easing”). Then, everyone will parse the FED chair’s announcement in an effort to discern the state of mind of the policy makers, whether they see something better or worse in the data than the rest of us and so on.

What the FED Will Do

My expectation is that this week the FED will (1) confirm that it will continue slowing its bond purchasing program and (2) confirm that it will raise the federal funds rate by half a percentage point (called “50 basis points” in finance-speak). Finally, it’ll also announce that it is watching inflation closely and will aggressively raise rates at future meetings if the economy remains strong and inflation high.

Nothing, however, is for sure. The above is the middle-of-the-road scenario and the one I assign the most probability to.

I also assign a real chance to them coming out more aggressively. Inflation continues to remain high and consumer spending continues to remain strong. US real GDP numbers showed a decline of 1.4% in the first quarter of this year, but that’s largely because consumer spending is outstripping domestic production. That caused imports to rise dramatically, worsening our trade deficit by 3%, and that’s counted as a negative in GDP calculations. If you look at just consumption plus investment in the US economy – sort of a measure of “core demand” – it rose 3.7%. The only problem is that a lot of that went to buy foreign goods.

In the aggressive scenario, the FOMC could raise rates more than half a point. That would shock everyone and send a shot across the proverbial bows of the global economy. I give this maybe a 20-25% chance of happening. And if it does, it’ll tell us that the FED sees inflation as being a lot worse than anyone is letting on.

There’s also a chance, say 5-10%, that they come out more tamely. They might do this if they are worried about China’s new Covid cases continuing to restrict supply chains, the war in Ukraine continuing to restrict supply chains and raise energy prices, and generally worry about a US recession.

It’s not clear what “tame” would mean here. FED Chair Powell has been saying they need to make serious progress on inflation and raising the fed funds rate is the key tool they use to do this. So perhaps tame will be reflected in his language and announcement of the policy decision. He might announce a more cautious approach going forward, that they are going to raise rates but slowly and contingent on developments in China and the Ukraine, etc.

What It Will Mean

The most likely outcome this week will be for the FED to follow the middle-of-the-road path. The effects of each piece – slowing bond purchases and raising interest rates by a half percentage point – are complementary but a little different with the increase in the federal funds rate getting the most attention.

Bond Purchases

Average people don’t see and feel a slowdown in bond purchases because it primarily affects financial markets and reserves in banks. The financial system is flush with reserves so there’s not going to be a sudden liquidity crunch.

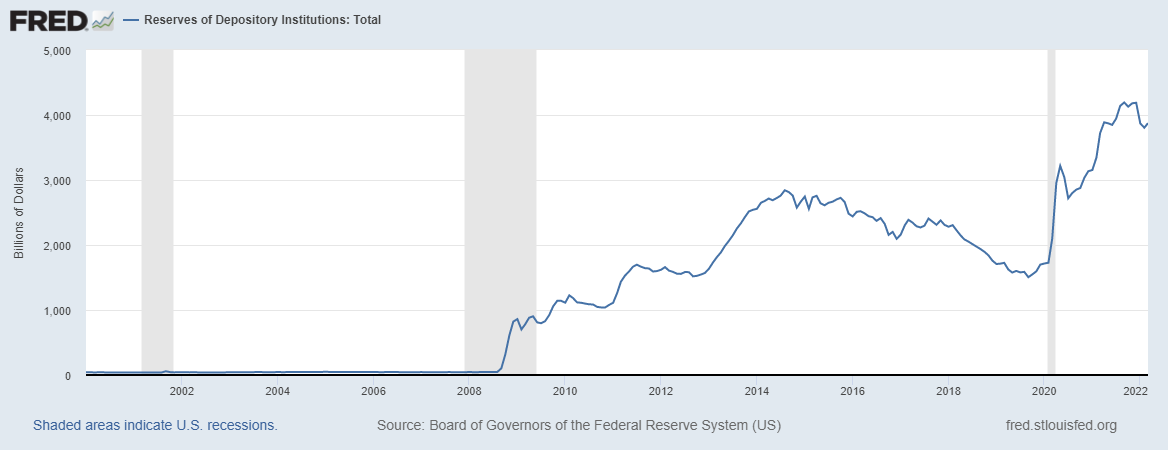

As seen in the graph below, banks didn’t hold much in reserves until the FED starting paying banks interest on the reserves they hold. Pay someone and they do more of it!

This started under FED Chair Bernanke in response to the 2007/08 crisis which was much more of a liquidity crisis, calling for a liquidity response. Since then we’ve switched our monetary framework to an “Ample Reserve Framework” which is what the FED now follows and that requires the FED to ensure lots of reserves in the banking system at all times as you can see in the graph.

We won’t likely see a huge drop in reserves, rather we’ll see a slowdown or cessation of their buildup. The last time the FED did this was around 2016 when the economy was growing and interest rates were normalizing.

The graph below shows both the funds rate (black line) and the reserves (blue line). Starting in 2016, the FED was raising rates and allowing reserves to naturally decline as the bonds matured. This is what they call “unwinding” the FED’s balance sheet. As the bonds mature, new bonds aren’t purchased and reserves in the system slowly decline as banks lend those reserves out but new reserves aren’t injected. This is most likely the plan going forward again and so we should expect reserves to slowly decline again over several years.

The interesting challenge, however, is that the last time this was done, the economy was growing (see graph below, real GDP in green). GDP was growing during the 2016 to 2020 wind down of reserves, but it will be shrinking over the coming year so banks will have a harder time lending due to reduced opportunities during the recession combined with higher interest rates causing a decrease in demand for loans.

The other effect of the decrease in bond purchases will be the effect on the bond market itself. As demand for bonds declines, the prices of bonds drop which raises the yield on bonds since bond prices and yields always move in opposite directions.

The increase in bond rates has already begun as seen below with 10-year (blue) and 2-year (red) rates already rising. The shorter rates are rising rapidly because of rapidly increasing inflation as well. To offer a positive return, the rate needs to be higher than inflation (otherwise your money is worth less and less over the life of the bond). The expectation is that inflation will be under control over 10 years and ideally back around the 2.5% target level so 10-year rates may not rise as rapidly but they should be higher than short-term rates in general so eventually they should settle somewhere a percentage point or two higher than 2-year rates. But that might not happen for another year or so.

As bond purchases slow, demand for US treasuries will continue to slow and rates should continue to rise. As mentioned above, the bond purchases are more about maintaining liquidity and ample banking reserves and so the slow down is less noticeable unless you are a bond trader or a banker.

The Federal Funds Rate Hike

The rate everyone watches is the federal funds rate. This is the interest rate charged in the over night market – called the “federal funds market” – where banks trade liquidity between themselves.

Think about the federal funds rate like the cost banks pay for their funds. When the cost of those funds rises, they have to charge higher rates when they give out loans in order to maintain their profit margins. By raising the federal funds rate, the FED raises the cost of lending which pushes up the lending rates too.

As the interest rate rises, consumers have an incentive to save a little more and hence consume a little less. This directly slows demand for goods and services in the economy. As businesses see less demand, they buy less inputs and this lowers demand for other goods in the economy. It’s this chain reaction that lowers overall demand in the economy, called “aggregate demand”, causing prices to fall or stop rising in all markets. That is the slowdown in inflation the FED is after.

For businesses higher interest rates also raise the cost of investing in capital and equipment. As investment slows, that causes an additional chain reaction of less demand for cement and wood and other things that goes into physical investment.

Again, those two key components of GDP, consumption and investment, are what were still growing strong in Q1 this year at 3.7% as mentioned earlier. So the FED’s goal is to slow those both in order to slow demand and slow inflation. The trick is to slow consumption and investment enough to slow inflation but not enough that business have to lay off too many people although the ugly truth no one wants to discuss is that slower growth means more unemployment too.

Three Unexpected Consequences

The interest rate increase has three other effects that need to be kept in mind: it will slow the stock market, strengthen the US dollar, and worsen the federal government’s budget situation. Each of those topics is worth writing about separately. Here are just a few notes to keep in mind and watch for in the news this week.

The Stock Market: As explained above, the decrease in FED demand for bonds combined with higher interest rates will raise the cost of money (consumer loans, businesses borrowing for investment, etc.) and will slow GDP. That means businesses are worse off and hence businesses’ stock prices will reflect that. Additionally, higher interest rates tend to make investors think twice about each investment and err on the side of caution which usually means moving out of risky stocks and into more secure investments. Stock traders don’t like higher interest rates and I do expect this to be a rough year for them.

The Strong Dollar: When interest rates rise, other people in the world want to move their money into the US to earn those higher interest rates. If you are in Europe, for example, and the interest rate is still near zero (which it is), your money isn’t earning you much. But if the US economy starts paying 3-5% returns, then you want to sell your Euros, buy US dollars, and put your money into the US to earn the higher return. That is more demand for US dollars which strengthens the value of the dollar.

The only policy problem with a stronger dollar is that it also makes all foreign products cheaper for Americans and encourages our consumers and businesses to buy foreign goods instead of domestic ones. This drives up imports, worsening our trade deficit. The US dollar has already been gaining in strength and our trade deficit has already skyrocketed. This is not sustainable. We can’t have high inflation, a stronger dollar, a looming recession, and an ever growing trade deficit. Something isn’t adding up. Watch for discussion around these topics.

Politics and Government Finances: The government has been running exceptionally large deficits in recent years and borrowing more and more money. The US government now has debt over 100% of GDP that it finances by constantly rolling over short-term debt. That’s like paying last month’s credit card bills with your credit card this month and then planning to do the same next month. It works for a little while but gets expensive quickly. And as interest rates rise, it will get very expensive even more quickly. That can only be reversed eventually by raising taxes and/or cutting government spending and that lays the perfect groundwork for political fighting. Combine that with a mid-term election year and we’ll hear more about this for sure.

Many commentators over the years have likened “easy money” to alcohol. It makes you feel great at first but the hang over can be rough. Some people liken the FED’s rate hike to “taking away the punchbowl” of alcohol at a party forcing everyone to sober up. Those are apt analogies.

The FED’s rate hikes are painful. Everyone loves the easy money. It’s cheap, abundant, initially you feel richer and can buy more stuff. The problem is that it leads to inflation and the only way to stop inflation is to stop the easy money policy and raise interest rates. We are about to hit the hangover phase and this week’s FED meetings will be a reality check for a lot of people, politicians and businesses around the punchbowl.

References

“The Fed’s “AmpleReserves” Approach to Implementing Monetary Policy”, Finance and Economics Discussion Series 2020-022. Washington: Board of Governors of the Federal Reserve System, 2020, https://www.federalreserve.gov/econres/feds/files/2020022pap.pdf

For the latest on the FED’s bond purchases, you can always check the NY Fed’s site (here: https://www.newyorkfed.org/markets/treasury-reinvestments-purchases-faq ) since the NY Fed is the one that conducts these trades.