Global Econ Q&A: Supply Problems and Inflation

Thank you to everyone who asked me follow up questions after my last column (Four Countries and Three Theories: The Modern Inflation Mystery[1]). The most common question was about the role of supply shortages in driving current inflation.

Some of the questions came from readers in Europe. Some from readers in the US. The answer is generally the same but the supply-side effects are much bigger in Europe these days than in the US. I’ll try to give some insight into the situation on both sides of the Atlantic.

And, I included a graph and some links at the end because on European reader asked if there are other metrics or graphs for supply challenges.

Supply and Supply Chains

We all see that there are still supply chain bottlenecks and shortages out there in markets. The question people have in mind is essentially “how much are these supply problems driving inflation?”

Right off the bat, let me say that supply side issues do restrict supply and lead to some higher prices. If they are broad enough, they can lead to higher prices in general (i.e., short-run inflation). And, that’s what most central banks thought they were seeing in summer 2021.

At that time, Covid was ending, supply chains were still messed up - so supplies were still short - but demand was returning to normal. That’s a clear recipe for higher prices.

The US Fed famously called higher prices in summer 2021 “transitory” for exactly that reason. They thought it was mostly a return to normal demand post-Covid and but in a world with still-restricted-supply. As those supply problems eased, prices should have fallen after the summer. That turned out to be wrong. Prices rose.

Since summer 2023, as supply normalized and global supply chain issues improved, inflation got worse, not better.

In Europe – and also in the US, but to a lesser extent – the Russia-Ukraine war has led to additional supply problems and led to especially bad supply problems in energy markets. This is because of past European mistakes in developing energy supplies that clearly made Russia a near monopoly supplier to the continent.

Any Russia-Ukraine war and Russian energy pullbacks would have been disruptive to be sure. The problem is that Europe set themselves in the most fragile position they could so that an energy problem is now an energy crisis.

Because many European countries have used price controls, Europeans are seeing many more empty shelves these days than we see in the US. So supply shortages seem more acute in Europe. They are more acute. But additionally they are perceived as being worse due to price-control-driven shortages too. See my earlier column on the issues with Price Controls[2].

Are there still supply problems?

Are there still supply problems? Yes.

Are they making current inflation worse? Yes.

That negative supply effect is worse in Europe and some other countries – any country that was reliant on Ukrainian grain and other products, for example - but inflation is also rising independent of the supply-side issues.

Prices rise because demand increases (holding supply constant) or supply decreases (holding demand constant) or demand increases faster than supply does. Supply and demand are like the two blades of scissors cutting paper. It’s hard to distinguish which blade cut more.

Part one of the story - a little more supply focused

Supply constraints raised prices. Massive government stimulus, especially financed by printing money, raised demand and that raised prices too.

But the timing tells us something. Early on in Covid, demand shifted from traditional purchasing patterns to new purchasing patterns. To state it in the extreme: we quit eating out in restaurants and we all bought too much toilet paper for some reason. This led to massive relative price swings. One price went down (restaurant-related services) and another price went up (toilet paper and cleaning supplies).

And, to be fair, that also fed through the system. For example, demand for home repair and related items rose dramatically as we all decided to make the best of work from home by also doing those home repair jobs we long neglected. Wood prices shot up. Windows and doors were delayed for months. And those price increases meant new home prices rose and so on.

Those demands on global supplies were dramatic. It was like saying “hey Bob, I know you work as an engineer. We don’t need those now. Can you be a doctor instead?” and poor Bob immediately enrolls in medical school. You see why it might take awhile to get supply restructured just because demand turned upside down overnight.

Conceptually Bob’s struggle is what suppliers around the world faced (albeit a little less dramatically). It takes a long time to change orders, change production, and then ship these things across the ocean from, say, China. So we saw shortages immediately and prices spiked up. … for some goods. Again, we switched away from other stuff which then became dirt cheap and in surplus.

And, it took awhile for those supply chains to re-adjust as demand returned to more normal patterns as lockdowns eased and people returned to life. Of course, add to that continued periodic shutdowns in China and elsewhere and all the other challenges in world and you get the complicated world we face today.

But those initial Covid-related supply problems are long gone. They were unwinding and correcting last year. Things are not perfect – they never will be – but they improved dramatically over the last year.

So Covid-related supply problems driving up some prices should be largely done. And, they were relative price effects. Some prices spiked up, others dropped. Overall prices – the price level – won’t move too much. Think of it as an average of all the prices. Some rose, some fell. The average might go up some or down some. It’s hard to say. In hindsight it looks like it went up.

But all this means that throughout all of 2022, those supply problems easing should be lowering prices around the world, not raising them. Supplies may still be low, but the improvement over this year should clearly be slowing inflation, not speeding it up.

The demand side

After summer 2021, prices continued to rise in the USA and most other countries.

That seems to have come from the tidal wave of money injected into most economies by their governments during the Covid pandemic. There is a known delay in its effect and the 2020 injection seemed to be showing up around mid 2021 and the 2021 injection (in the US) seemed to be showing up around mid 2022.

But IF THAT’S RIGHT, then we should see less inflation in 2022 for those countries that did not inject more money in Spring 2021 (like we did in the US with our second stimulus bill). But we do see inflation in the other countries! And it’s getting worse, not better.

And that’s part of the mystery. Every time it looks like a clear, simple answer (some “obvious” cause and effect), something else doesn’t add up and it’s back to square one.

Back to the supply side

Perhaps what’s happening is that the other countries got a second supply shock: War in Ukraine. This is causing huge energy problems in Europe and massive energy price spikes across the continent.

When I wrote my last piece, I was thinking that, if that’s the cause, then we should see stronger effects on the continent than in the UK. My logic was that the UK had its own energy arrangements and the continent’s arrangement is largely driven by bad German choices to lock into Russian supplies.

But that may be wrong. As I’ve been reading and thinking, I’m learning that the UK may have had unique energy policies that left it more susceptible to these prices swings in gas prices while some Europeans like the French have nuclear backing them up. So, I don’t know. I need to look deeper.

The Mystery

This is the mystery: what’s driving inflation and driving it now? Why did it break out everywhere? One answer is Covid. Okay, but then what aspect of Covid? The demand drop, then recovery (and over-stimulus)? Or the supply drop, then recovery? Both? Can we even untangle them?

If it was supply, then prices should FALL as supply recovers. So supply could have explained higher prices last year, but not now. At least not in the US.

I personally do not think supply is driving inflation in the United States. Period. Full stop.

That being said, there are competing economic theories for the demand-side causes of inflation and it’s not clear which one is right any more. That’s what I was writing about in my last column and what I’ll continue to dig into.

But, it might be that the US was hit by a negative supply shock (causing higher prices initially), then a delayed positive demand shock from all the stimulus (causing higher prices later) and now both are fading.

At the same time, Europe faced the same supply and demand shocks (minus a second massive spending spree in 2021), but now when things should be improving like in the US, Europe is hit with a second wave of supply shocks, mostly in energy and other war-related markets.

That story seems to make a lot of sense. It is and will continue to be very appealing. My guess it we’ll hear it more in the papers as others come to a similar realization.

But then I have a serious problem: Why is the US Fed raising interest rates? According to the story I just told above, inflation is going away on it’s own. The two shocks are largely over, at least in the US.

Maybe more relevant: Why is the Bank of England and now the ECB also raising rates? They can’t fight a supply shock. Raising rates (restricting demand) will make the negative consequences of a supply shock worse!

So the policy makers do not believe the one-two hit US and one-two-three hit Euro story at all. They believe their excessive money and excessively low interest rates are driving inflation.

Back to square one. Again.

Appendix: Some links and graphs

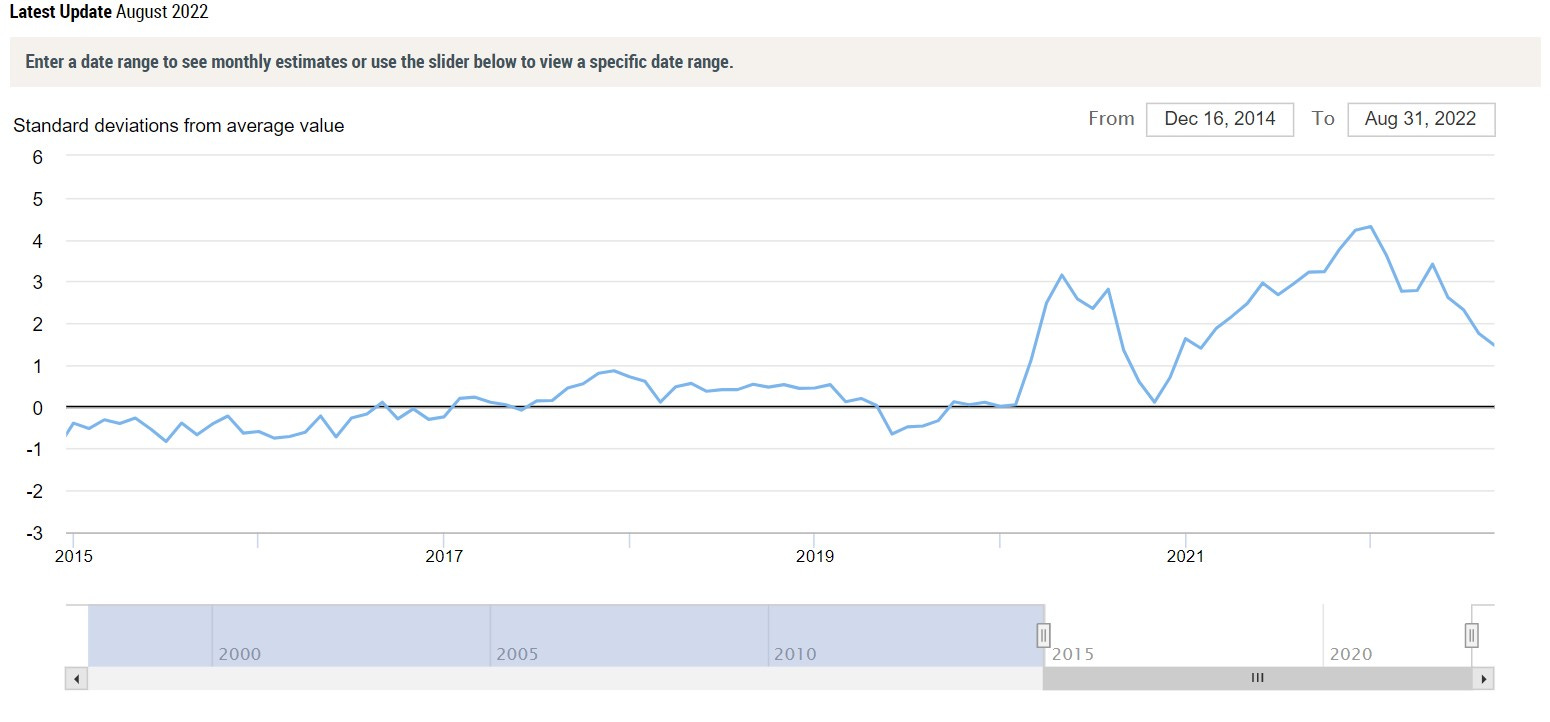

One person asked for any good graphs and links about supply shocks. There is a cool one developed by the NY FED called the Global Supply Chain Pressure Index (GSCPI)[3].

From the Fed’s site:

“Estimates for August 2022

· Global supply chain pressures decreased in August, continuing the easing observed over the past four months.*

· The August decline was quite broad-based, with decreases in delivery times recorded for all the countries in the sample. A decline in backlogs in the United Kingdom also made a significant downward contribution to the index.

· The GSCPI's year-to-date movements suggest that although global supply chain pressures have been decreasing, they remain at historically high levels.”

In other words, as we also see in the graph, supply chain problems peaked and have been improving since at least the beginning of 2022. During that time, even if delayed a bit, this should have had a deflationary effect (at least in the USA). So it shouldn’t be the driver of the inflation we’ve been trying to battle this year.

The developers of the index have a great article discussing it and other, alternative measures that focus on specific aspects of global supply chains. I highly recommend it for the interested reader: A New Barometer of Global Supply Chain Pressures[4]

[1] Global Economics. Four Countries and Three Theories: The Modern Inflation Mystery:

[2] Global Economics. The Problem with Price Controls:

[3] GSCPI: https://www.newyorkfed.org/research/policy/gscpi#/interactive

[4] NY FED Liberty Street Economics Blog: https://libertystreeteconomics.newyorkfed.org/2022/01/a-new-barometer-of-global-supply-chain-pressures/