Milei’s economic ideas aren’t so crazy for Argentina

World headlines have been full of news of the “radical/right-wing” libertarian who won Argentina’s primary vote for President, Javier Milei. Most of the news focuses on his proposal to close the Argentine central bank, and switch the country to using US dollars followed by bits and pieces of the rest of his policy agenda, all to show he’s a bit crazy, and would crash the economy.

I don’t know too much about Mr. Milei. I tried hard to figure out what is meant by “right-wing” libertarian, a term I hadn’t heard. But I do know a little about Argentina, and monetary policy, and his idea is not crazy.

Dollarizing the economy is neither new, nor particularly radical for Argentina. Dollarizing also often includes “closing the central bank” which can mean many things. As for his other views, you can read about them on his Wikipedia page. It looks like it’s being updated daily.

Javier Milei

Very briefly, a few things about Milei seem relevant. First, he’s relatively new, but was already in politics. He has been in the lower house congress since 2021 and heads Liberty Advances (La Libertad Avanza) which is a political coalition of “right-wing” parties.

In the current political world, I don’t know what any descriptions mean any more, and I am certainly not an expert on Argentinian culture and politics. So, I leave it to you to read, and make up your own mind. I write this as an American, where half the country calls any Democrat a socialist or communist and the other half calls any Republican a fascist or neo-Nazi. So dipping our toes into interpreting political speech in other countries should be done with a little self-awareness and caution.

On his economic views, and the Argentinian economy, I can speak with a little more confidence.

He does hold degrees in economics, and worked both as an economist in the private sector and as an economics professor. His specialty was macroeconomics, monetary theory, and mathematical economics. He apparently identifies as a liberal-libertarian or a “miniarchist” which apparently means someone who thinks there should be a minimal state. Ask a libertarian friend about these definitions. The libertarians seem to have lots of subdivisions of views, each with its own label. In any case, those are the views he self-identifies with.

Finally, he’s had a radio show, and a very public, popular presence for some time, and seems to have a talent for stirring up controversy. Even on a personal level, Bloomberg comments that he is single by choice, and has five 200-pound English Mastiffs named Conan, Murray, Milton, Robert, and Lucas after “The Barbarian”, “The Libertarian”, and two famous economists.

Latin America: A Macroeconomic Experimental Lab

Latin America has long been an experimental lab for monetary policy. It is a region of hyperinflations, debt crises, fixed currencies, floating currencies, mixed fixed-floats, multiple currency regimes, dollarization, and bit-coinization too!

There’s a reason so many great macroeconomists come from Latin America like Manuel Sidrauski, Guillermo Calvo, Carlos Vegh, Sebastian Edwards, Martin Uribe, and Carmen Reinhart to list only very few of the top. I would add to that list – and most in that list would agree – the late Leonardo Auernheimer, my PhD advisor, who was an Argentinian.

In Latin American economies everything seems to be taken to extremes. If you believe in fiscal policy, then the whole economy gets moved to a socialist-communist state. If you believe in free markets, you move to the opposite. You can even mix and match, like the Chilean Pinochet regime that was a military dictatorship yet promoted free markets for about 20 years. Like I said, a macroeconomic experimental lab.

Inflation Problems

One persistent problem in Latin America, however, is inflation. It comes and it goes, only to come back again. And, when we discuss inflation, put away your modern American or European thinking caps. 10% inflation was often seen as a blessing in this part of the world where inflation hit thousands of percent a year in the 1980s.

Today in Argentina, it’s reported at 119%, and the concern is that it will get further out of control due to massive government spending that already bankrupted the economy, putting it back under IMF programs. Now it looks like it can’t afford to repay even the IMF loans, leaving it’s economic outlook bleak for the coming years. This is serious.

Despite all the controversies I normally discuss about causes of US inflation of 3-4% today, there’s almost zero debate in economics that high inflation (and definitely hyperinflation) is everywhere and always a monetary phenomenon, to quote Milton Friedman, and, most of the time, that’s driven by fiscal policy that got out of control, blew up, and left the government trying to print money to pay its bills.

Inflation Solutions

There is one fundamental solution to an economy’s inflation problem: policy discipline. Ideally, that comes from responsible fiscal policies coupled with responsible monetary policy. If those two things are in place, we can debate if 0% or 2% or 5% are the right targets for inflation, and what the main drivers are that bounce it around annually. Those are “low inflation” debates.

The debate in Latin America is often a “high inflation” debate. The problem has traditionally been institutional. I’ll look at three monetary regimes that also provide institutional solutions. There are other regimes out there, but these are the main ones.

Solution One: Money Growth Rule

The idea here is that the central bank forecasts real GDP growth over the long run (i.e., how fast the supply of stuff is growing). If the central bank printed money as fast as real GDP grows, then supply and demand grow equally fast and inflation would be zero. But generally central banks aim for 2% or so inflation, so they print money 2% faster than real GDP should be growing. In theory, the central bank would turn on the printing press at that rate and go home, maybe meeting once a year or every other year to see if they need to change their forecast of real GDP growth or not. That’s it.

The ”going home” part is the institutional solution. The idea is that, if the central bankers stay in their offices day to day, looking at data, they will be tempted to tweak things and pretty soon they’ll also succumb to political pressure to print more (stimulate the economy) around elections, print to pay government debts, and in no time hyperinflation will be back. So, set a rate, turn on the printing press, and send everyone home.

I’m stating it in a bit of a caricatured form, but the idea is what’s important here.

In theory and in practice this works to take an economy from hyper to normal inflation. Once inflation is low, there are a host of issues around inflation annually, and, in the extreme form I describe above, it’s politically difficult to maintain. How can we have a central bank with employees whose job it is to stay home? Inflation this year is a little higher than normal, can’t they do something now? Must we really wait until they re-adjust things in a year? You can imagine the news coverage!

Solution Two: A Fixed Exchange Rate regime

The exchange rate between, say, the Argentine peso and the US dollar is how many USD you need to buy 1 peso, or how many pesos you need to buy 1 USD.

Inflation erodes the value of a currency. If one of those currencies inflates, its value erodes faster than the other one, and the exchange rate moves. If the peso inflates, then you need more and more pesos to buy food, clothes, etc., and you need more and more pesos to buy USD. The last one - pesos buying USD - is the exchange rate.

If I fix, say, the peso’s value to the USD, then my central bank is guaranteeing that you always need exactly the same number of pesos to buy 1 USD. The value of the peso is tied to the USD, and cannot rise faster or slower than the USD. That means, peso inflation will have to be exactly USD inflation. In this way, Argentina (or any country) can unilaterally fix their currency to the USD, and adopt US inflation.

It sounds crazy, I know. But this was actually the single most common monetary regime for most of relatively modern history after using gold and other metal coins themselves as currency (called a commodity currency system). Countries either fixed the value of their currency to a commodity, like gold, or to another currency. In this way, they adopt either gold’s inflation rate, or the inflation rate of the other currency.

In its caricatured form, you fix the currency, and also send all the central bankers home. It has a similar institutional benefit to that of the money rule in removing the people and political motivations from the equation.

There are, however, additional political/institutional benefits as well. With a money rule, average people don’t see the money supply every day. So it’s hard to feel and see that the central bank is doing anything.

Everyone uses their currency every day, however. They can see that the value is 100% fixed to, say, the USD. They can check it in the newspapers, they can see it in stores, they can see it when they travel, trade with other countries, etc. It’s very visible.

One big problem, however, with this regime – even in its idealized form – is that your country must have a huge stock of USD in reserve. Whenever you fix a price[1], quantities do all the adjusting. In this case, you fixed the peso price of USD, so you must have an unlimited quantity of USD to buy and sell at any time in order to keep that peso per USD price constant.

If you run out of your USD reserves, you can’t buy and sell, and, therefore, can’t maintain the fix, and the system collapses. The world and history is full of examples of this. It has led to the downfall of nearly every fixed exchange rate regime in history with few exceptions (for one example, see “Fixing to adopt the Euro” below). It’s why the Bretton Woods’ fix to gold collapsed as well.

Fixing to adopt the Euro: The EU countries all fixed to each other, collapsed in 1992, but then in 1999 they adopted the Euro so that’s not a collapse. And since 1999 each country wanting to join the EU is required to eventually adopt the Euro. To do that, they fix their domestic currency to the Euro for a period to force their inflation rates to align before adoption. So those aren’t collapses either.

Finally there’s one other political/institutional issue. That is, politicians always want the central bank to change the fix, just this once. If the economy slows, the central bank can adjust the fix just once, saying okay, instead of 1 peso for 1 USD, we’ll make it 1.1 pesos for 1 USD. That is in effect 10% inflation which requires 10% more pesos to be added to circulation. That is a 10% increase in the Argentine money supply, and stimulates the economy in the short run.

Of course, if you can do it once, then you can do it twice, three times, and so on. That’s a slippery road back to hyperinflation. Additionally, if the fiscal side of the government hasn’t behaved, it turns out, the central bank will lose USD reserves at the exactly same rate as government’s budget deficit (5% a year, 10% a year, and so on as things worsen). This hastens the system’s collapse.

One institutional solution to this is to send the central bankers home, and establish a “currency board” whose sole job it is to make sure the fixed regime continues, monitoring how much reserves there are, etc. This makes the political pressure more costly, but doesn’t fix it. And, it doesn’t fix the problem of losing reserves when the fiscal house is out of order. Some countries then even adopted a “fiscal board” as well, establishing a panel of experts to monitor and control fiscal discipline. Now you’ve outsourced your monetary and fiscal policy, and sent as many political actors “home” as possible, because they can’t be trusted to manage things.

When fixed regimes collapse, you generally see huge bouts of inflation, frequently bursts of hyperinflation. You see a fix with low inflation, then more and more “adjustments”, more and more inflation, then usually a last-ditch effort to not adjust again, so inflation is constant again briefly. Then, the whole thing collapses and inflation jumps to, say, 100% or more for a year.

Solution Three: Inflation Targeting Regimes

Starting in the 1990s, a new regime became popular, because it seemed to solve the institutional problem. Inflation targeting regimes require the fiscal side of government (i.e., congress, parliament, etc.) to pass a law that establishes an inflation target, and a whole inflation targeting regime. This law usually says that the central bank must meet this target, say 2% a year, no matter what, and must publish monthly inflation reports that are public.

In principle, the law shouldn’t care how this is done, but generally today central banks establish and publish their interest rate rule showing how, when, and by how much they raise or lower interest rates in response to inflationary pressure.

Other stuff can be added to the target like unemployment or output. That’s quite common. But there are also some “strict inflation targeting regimes” that don’t care about those things at all, focusing solely on inflation instead.

These worked wonderfully throughout the 1990s, first in New Zealand, and other advanced economies, then across emerging markets as well, including many in Latin America (in Mexico and Chile, to name two prominent examples). Professor Ben Bernanke was a prominent scholar of inflation targeting, and even co-authored an excellent book reviewing the history and documenting the successes. When he was Fed Chair, Bernanke openly started moving the US Fed toward an inflation targeting regime. Then the Great Financial Crisis hit, and everyone’s focus changed.

Suddenly, central banks needed to do a range of things other than just fight inflation. They had to manage banking systems in a new way, buy bad mortgages, and expand liquidity regardless of the inflationary effects. Attention got diverted and since then interest in pure inflation targeting regimes has waned.

What all three of these regimes - money rule, fixed exchange rate, and inflation targeting - have in common is a distrust in politicians, or, more precisely, a recognition that there are real-world political incentives that can lead to outcomes that we didn’t intend. Economists call these Public Choice problems and there’s a vast and fascinating literature on the subject. These regimes are all efforts to solve the incentive, public-choice challenges of conducting monetary policy, and most of them include some version of “sending the central bankers home”.

Dollarization and Truly Sending The Central Bankers Home

Now we get to Melio’s suggestion: adopt the US dollar in Argentina. It sounds crazy at first, but it is not. An extreme way to fix your currency is to dollarize. Why hold a stock of USD and try to keep your own currency too? You might face collapse anyway if your fiscal authorities can’t control themselves. And, as long as it’s a fixed exchange rate, there’s a temptation to adjust, as we discussed above.

Instead, just adopt the USD as your country’s legal tender. Close the central bank and you are done. Inflation problem solved, permanently.

Of course, as mentioned in the example of adopting the Euro, there will need to be an adjustment time. One solution is to fix the peso to the USD, adjusting a lot at first (since there’s a lot of inflation) but adjusting less and less until after, say, a year and then the fix remains unchanged. Argentine inflation and peso inflation will be the same and then you can switch the currencies out completely, like adopting the Euro.

Milei correctly – in my opinion – recognizes the political dangers of this. First, Argentina had a fixed regime for many years. People might see him as returning to it. Second, and more dangerous, is that, once established, it’s hard to kill any government program, and a “temp fix” would be no different. The political mood might shift, might push for a longer transition, and support might even build to keep the fix.

Milei’s solution gets around that. He leverages free-markets which he promotes in every sphere of the Argentine economy, making this proposal part of a consistent package. He would allow people to choose to use either USD or pesos. It’d be their choice.

This approach allows him to make the USD legal tender on day one while he has political wind in his sails following a win of the presidency. Then, we know people will choose the more stable currency. Over a few months, the USD would be used more and more, the peso less and less. At some point, Argentina would just quit printing pesos. Pretty clever implementation strategy in my opinion. In practice he’ll have some challenges, but it’ll be very interesting to watch and should succeed if he has a little political support for it.

Dollarization Successes: El Salvador

In January 2001, the USD became the legal tender in El Salvador along with the colón, the domestic currency. The central bank stopped printing the colón altogether in 2004, and even made Bitcoin legal tender as well in June 2021.

Why would they do this? Here’s their inflation history.

It’s been better on average since 2001. Of course, US inflation took off after 2020 and that means El Salvadorian inflation did too (see end of graph). If you adopt a foreign currency, you adopt their inflation for better or worse.

Dollarization Successes: Ecuador

Ecuador also dollarized in January 2000. You can see their inflation history too.

Post 2000, inflation has basically been the same as it is in the US, permanently solving their inflation woes.

The longest example I know of is Panama. Panama adopted the US dollar as its currency in 1903.

Other countries have adopted other currencies. Those joining the EU adopt the Euro and drop their national currency, albeit for reasons other than hyperinflation. This general phenomenon is called “currency substitution” and those interested in reading more can find lots of information and links on Wikipedia: https://en.wikipedia.org/wiki/Currency_substitution

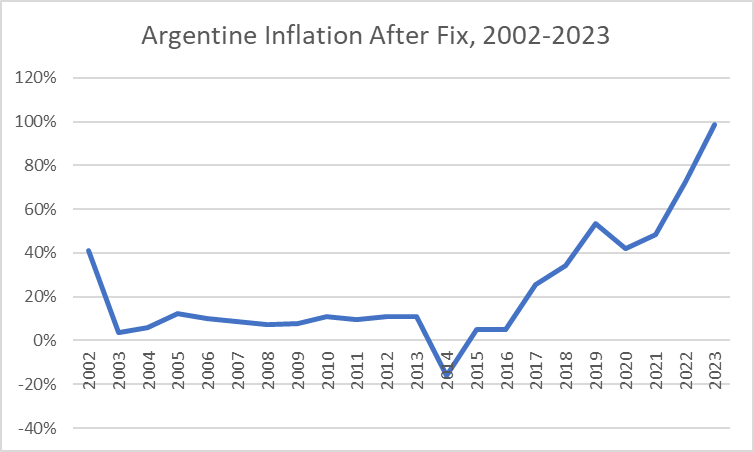

Argentina’s Inflation History: The Case for Dollarization Today

The inflation spike in Ecuador was less than 100% a year. In El Salvador, it was about 100% a year. In Argentina is was about 5,000% a year. That was in the 1980s, but Argentinians remember that.

It looks like it disappears right after that. What happened?

Well, they “dollarized” in 1991. It was called that at the time, but it wasn’t a pure dollarization. It was technically a super hard fixed regime that had a currency board and all the institutional trimmings to keep it in place. Inflation dropped like a rock, but the fixed regime collapsed in 2001. They’ve had inflationary problems off and on since, and problems have gotten progressively worse in recent years. Argentinian inflation today is over 100% again.

Graphically some of that is also scaling. On one graph, if the peak is 5,000%, then even 100% later doesn’t register as a blip. Below, I show inflation from 1991 to 2001, the period of “near dollarization”. I removed 1990 because inflation was still 1,300% and it ruins the graph again. In any case, you can see inflation dropped like a rock.

This was a successful period for Argentina and it was used as a successful, but debated, example at the time. A lot was written about Argentina fixing the currency at the wrong value, leading to an real exchange rate that was overvalued. I won’t go into that, but it’s just to tell you that there were criticisms of technical details of the regime that mattered, and are believed to have caused lower growth, more unemployment, etc.

Milei would know all of that well. His solution therefore is designed to get the inflation benefits without those problems.

The “near-dollarized” regime, like most fixed exchange rate regimes, did collapse in 2001. Inflation rose, then fell again, but has been rising again in recent years.

You can see that somewhere around the 2015-2016 period, things changed again and Argentina has been on a bad inflationary path ever since. To put this in perspective for all my US and European readers, we have been suffering – just think about your own experience – with inflation of around 10% for the last two years. Some countries, like Hungary, are still struggling with 20% inflation today (unacceptable, in my opinion).

In 2017 – pre-Covid!!!! – inflation was 25% in Argentina, rising to 34% then 50% and around 100% today. That is a longer and much worse and now worsening inflationary situation.

Conclusion

Given Argentina’s history, no wonder they are considering radical solutions to fix it once and for all. With everyone poking fun at Milei in the press, particularly calling his dollarization plan radical, and painting it as crazy, I wanted to explain the situation.

It sounds crazy from a US or European perspective, but not from a Latin American or even a global one. I think it’s a good idea, and his implementation policy is a clever one, similar to ones used in El Salvador and elsewhere when they introduced new currencies. So, it has precedents, too.

I don’t know anything else about Milei. He might be a good candidate or not. I do not know. What I do know is that his dollarization proposal makes sense and won’t sound surprising at all to anyone in Argentina or the rest of Latin America.

APPENDIX: Argentine Inflation in Numbers

1991-2002 was the “hard fix” or “near dollarization” period and 2015-2016 are when I don’t have data and use estimates. The data mixes Fred data and IMF data and is what I used to make the graphs in this column. Note that other estimates today say 2023 inflation is 119% in Argentina. Here I use IMF data (maybe older) estimating it at 99% for 2023.

[1] See my other pieces on fixing prices. This is a universal thing regardless of whether you fix the price of currencies, cars, gas, housing, wages or anything. “The Problem With Price Controls” (July 15, 2022).

This is a very well written piece. I think the key thing to remember is that Argentina is just in a terrible economically and politically. As you talked about, its inflation is just completely nuts, and some radical changes to need to happen to its economy to stablize its currency; dollarization is a pretty good option imo. However, I think it's a little unfornuate that an "anarcho-capitalist" is the only one that is willing to do it. Strict idealogues are generally bad news for a country, and anyone who considers themselves an "anarcho" anything should be keep as far away from power as possible. Argentina is essentially forced to choose between that and more of the same 'Peronist' economics that has rotted their economy.

Hey, maybe Millei will embrace pragmatism and suprise me, or otherwise be constrained in his efforts to implement by Argentina's political system. Maybe he even has the magic fix to Argentina's woes. But as for now, I'm not looking forward to Argentina's next election.

Thanks. That's an excellent point. Again, it was done for slightly different reason, namely to join the Euro area versus because the local country had 200% inflation or something. But very good point. Thanks and thanks for reading