The Upside Down World of Government Recessions

We all have credit cards these days. Access to credit allows us to manage our current spending somewhat independent of our current income. Around the holidays, we often buy presents on our credit cards even though we likely didn’t get a sudden bump in our salaries. Why would we do that? Because we know our income is reliable and we’ll pay it back over the first few months of the new year.

When times are tough, we might use the card a little more. We’ve all been hit by that unexpected car or house repair bill that we had to put on a card. But if every month, we spend more than we earn, our credit card debt rises and rises.

At some point we have to make a choice: either we need to earn more income or spend less money.

Must we get to that point? Yes.

If your conditions don’t change, you can’t continue to borrow forever. Why not? Because people won’t keep lending to you. At some point they want to be repaid.

How would you know when you reach that decision point? What if someone isn’t the kind of person that worries about their long-term financial situation and never wakes up, so to say? Would they still realize they hit that point? Yes.

When I was probably 18 or 19 years old, a relative of mine filed for bankruptcy. The banks repossessed her car and other higher-valued items. A few months later, we were talking and she was mad. She had just gone to a car dealer, found a great new car but when the only loan they were offered was at 3-4 times the normal interest rate and required lots of money down, she got mad. “Why? That’s not fair”, she exclaimed. I was surprised they offered her a loan at all, but that’s a different matter.

At some point, whether we are aware of our situation or not, if we persistently spend more than we earn, we will all face that decision point because we can only borrow more money if someone else is willing to lend to us. They can see our income and spending pattern, form expectations about our future income and ability to repay as well as we can. They will only lend if they think they’ll be paid back.

As we near that point, the first thing that usually happens is the interest rates they offer us starts to rise. They will lend to us, but they need a little extra compensation for the risk. If we get offended, that’s fine, but they will just lend to someone else who is less risky.

If we get offended, then with no new money in hand, we face the decision point immediately. Either raise our incomes immediately or cut our spending and start paying back our debts. Of the two choices, realistically, our only option is to cut spending. If we can increase our income overnight, we probably would have already done that.

If we didn’t get offended and agreed to the higher interest rates, but otherwise continue down the same road without changing our income and spending, then our debt will begin rising faster than before as we roll over credit card debt each month but now at higher and higher interest rates, growing the total amount owed more quickly. This can postpone when we reach the decision point, but it’s clear that we’ll hit it again soon. And when we do, it’ll be worse than before because we have more debt at higher interest rates.

Now when we hit the sudden stop of credit, we’ll have to cut our monthly spending by even more, making our lives even harder than they would have been, had we changed our spending sooner.

The UK Announces Spending Cuts and Tax Increases

Looks like the government of the UK hit that decision point.

For a government, “income” is what it brings in from taxes. If it spends more than its income, it must borrow from someone. It does that by issuing bonds, something we as individuals can’t do. But that’s actually the least important difference between people and governments.

A more important difference is that there are no “bankruptcy courts” for governments. If a bank lends me money that I can’t pay back, I file for bankruptcy. The bank seizes some of my assets (cars, the house, and other valuables), agrees on some payment plan from me and the court likely docks my income to repay my debts. That is, the banks still get something.

But there’s nothing like that for governments. Lenders are therefore much more cautious when lending to governments. They look very carefully at their history of payment as well as their taxing and spending policies both today and in the future.

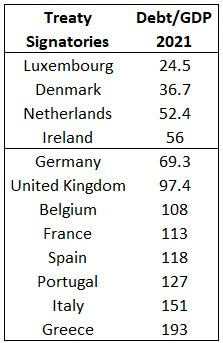

It’s very hard to predict in advance when a country will hit that decision point. International macroeconomists usually expect smaller economies to hit that point when their debt gets to around 80% of GDP. For sure we start to expect it if the economy hits 100% debt to GDP.

For that reason, the Maastricht Treaty, which founded the European Union, requires countries to keep government deficits at 3% of GDP or better and total debt at 60% of GDP or better. The idea is to limit the monthly borrowing in the first place (hence the 3% restriction) and set a total limit (the 60%).

The debt to GDP restriction of 60% tells countries that run deficits regularly that they have to keep the longer-term picture in mind. As they near 60%, policy makers in the country’s capital look for ways to improve the countries fiscal situation, get spending down, taxes up and avoid any really bad debt problems.

Those criteria were especially important to convince the big countries like France and Germany to get on board. They wanted to be sure that, once united with a single currency, the smaller countries didn’t blow their budgets and put everyone in danger.

The above table shows the debt to GDP ratios for all the countries that were the original signatories to the Maastricht Treaty, which is still in force today, by the way. Good think Germany and France made sure…err…well, never mind. Let’s move on.

For smaller economies, 80% or so was really a danger zone traditionally. With bigger economies, no one really knows where the limit is. But you know you are there when lenders eventually quit lending.

The UK Gilder Crisis

And this brings us back to the UK’s problems. When the Truss government, about a month ago, declared tax cuts and spending increases, lenders said “no”.

For the UK government, that meant lenders in the bond market didn’t want to buy bonds at the old interest rate. And that’s a first signal: interest rates rise. The government had to offer higher returns (“interest rates”) on their bonds to get people to buy them.

That is exactly the same as the credit card company saying, “we’ll lend you more but only if you pay a higher interest rate because you are more risky to lend to now”.

Whether the UK government, economic observers and commentators and anyone else felt that was justified or not does not matter. Like my relative’s protest and moral outrage, the choice is to take the money and pay higher rates or not.

If you look at the Maastricht countries again, you can see why the Truss government didn’t expect such a reaction. Look at France. The French government has 113% debt to GDP. Lenders haven’t turned on France.

The tax cuts and spending increases the Truss government proposed weren’t too crazy. Surely lenders would be okay with a few additional percent of debt to GDP.

Apparently not.

The UK’s New Policy

Liz Truss is out as Prime Minister and the new government has not only dropped that initial program but last week it announced a reversal.

On Friday, November 11th, the latest GDP numbers came out and showed that UK GDP shrank in the third quarter this year. That was bad news and yields on British bonds rose again. Why?

This is another difference between individuals and governments. People earn income by working or selling something or investing their money. A government can only[1] earn money by taking it from its citizens through taxes. But those citizens earn their money by working, producing, selling, and investing and all those activities together are the economy’s GDP.

This means that when GDP slows, the people in an economy have less and – for the same tax rate – the government will collect less revenue. A low GDP report is financially the same as announcing an income reduction for the government. And, usually, when GDP slows, government spending for things like unemployment payments also rises. So this is essentially another tax cut and spending increase announcement. The difference is that the government isn’t announcing it directly and is also less able to control it which is worse in many ways than announcing a bad policy which can be – and was – reversed.

This was followed by an announcement on November 16th that UK inflation reached 11.1%, a 41-year high. That is up from the 10% it had the previous month. Yields on two-year UK government bonds rose again following this news.

The UK government therefore announced the largest tax increases and spending cuts in a decade. And they did it in an interesting way that shows they are trying to convince lenders that their long-term financial prospects are good while trying not to worsen the current economic situation.

When the government raises taxes, it takes money from its private citizens, hence harming GDP directly. And government spending is buying something in the economy from a private person or business. So less spending also harms GDP directly, at least initially.

The spending cuts are set to begin in 2025 and the tax increases are coming by essentially suspending inflation indexing of taxes.

The delayed spending cuts are surely an effort to not worsen things today but show potential lenders that the government is committed to better finances down the road when, they hope, the economy is stronger as well.

The tax increases are a bit devious. When inflation rises and wages rise with it, everyone’s nominal incomes rise at the rate of inflation (let’s assume for simplicity). You may not feel richer because your paycheck is growing at the same rate as the price of the things you buy. You earned 10% more, but everything costs 10% more as well, so it washes out in real terms.

That’s all fine except for one lovely fact. Your higher income due purely to inflation puts you in higher and higher tax brackets with your government. This means that, during inflationary periods, governments often naturally collect more taxes as more people slip upward in tax brackets. Some governments raise those brackets with inflation – called “indexing” the brackets – and that is what the UK government just announced it will stop doing.

Oddly enough it’s sort of the gentlest way the UK government could raise taxes. Nothing will really change, just inflation will rise and push people up a bit into higher brackets.

This won’t be popular though. People will all rightfully see this as follows: the government caused inflation and, instead of helping us, now it’s taking advantage of it to get more money.

The UK government has little choice. Every politician would love to spend more to “help” citizens avoid the pain of a recession. But like my relative when she finally couldn’t borrow more, when you hit the financial decision point, the only choices are to cut spending and/or increase income. For a government, both come at the expense of its citizens.

The Upside Down World of Government Recessions

Reading the above, it all follows logically and should hopefully be clear. It’s not nice, it’s hardship all around, but it’s understandable. To see why I call this “upside down”, let’s flip it around for a minute.

This will give you some insight into the political debate as well as some discussions among commentators these days.

We all know that economic policy is supposed to help us during times of hardship. When we enter – or even just get near – a recession, the government can print some extra money, increase spending a little and maybe even cut taxes some, all to stimulate the economy and ease our burden.

That’s true. Governments can and do engage in such policies.

That is equivalent to using your credit card during tight times. It is absolutely fine, people do it, and it’s solid advice in general.

The problem is that, if you do it all the time, it becomes the problem itself. Now when you hit the borrowing limit you can’t “just put it on a card this month”. And if you try, things get even worse as we discussed above.

These fiscal/financial problems are usually the problems that emerging markets face. When the international lending to them suddenly stops flowing in, their economies collapse. It’s called a “sudden stop”, from the old banker’s adage that “it’s not the speed that kills, it’s the sudden stop”[2].

It’s apt here because the “speed” is exactly the speed of government borrowing, spending and printing money that got us all into the mess in the first place. Countries must therefore do the opposite of what they’d normally do in a recession. That’s why it feels upside down, from a policy perspective.

We’re All Watching With Bated Breath

All the major economies are in the same boat. None of us know where that decision point is and it can sneak up on any economy the way it did on the UK.

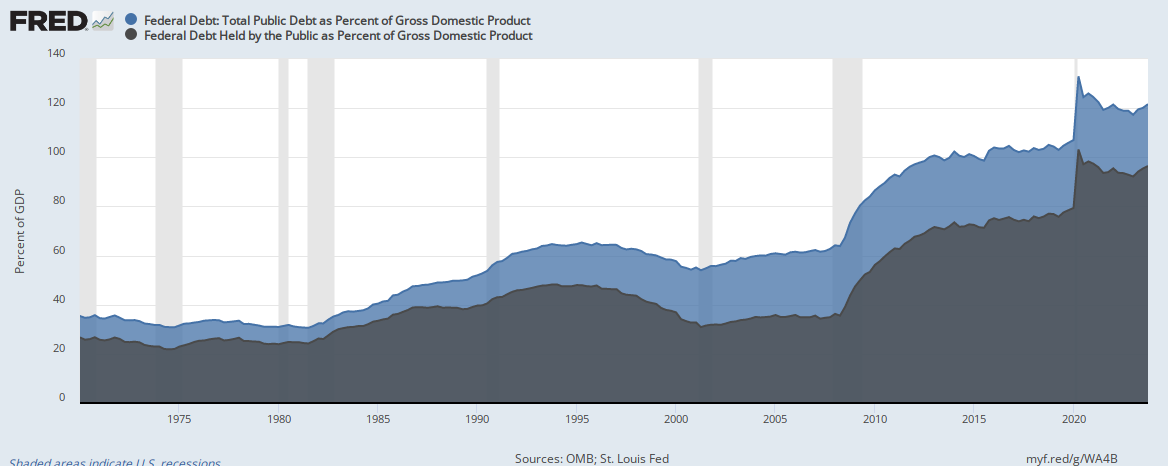

The US has 97% to 137% debt to GDP, depending on how you calculate it[3]. The EU members are around 95% debt to GDP, on average. Some are higher, some lower. Canada is around 100% as well. So we all worry that we are next. No one knows. It’s all up to how the lenders view our governments, GDP in the future, etc.

Japan has 262% debt to GDP and seems fine. This gives all the “advanced” economy governments hope. But that’s dangerous. We all know someone who smoked a pack of cigarettes a day and lived into their 90s. Still, it’s not good advice in general.

Inflation and debt problems come solely from governments. Individuals in an economy can’t generate them themselves. The reason it that individually they hit borrowing limits and what one person in an economy owes, they owe to another person in that same economy.

Governments are the only ones who can spend and borrow, based on the private citizens’ good credit. And their ability to borrow in world markets makes it feel costless to the citizens and hence makes it even easier to let things get out of control.

Governments are the only ones who can print money that everyone “has to use”. Try to pay the IRS with Euros. You can’t. And you can’t pay taxes in France with USD.

Funny enough, this is the Fiscal Theory of the Price Level. A country’s currency is issued by that country’s government. And in the end, it’s only as valuable as that government is reliable. When a government runs into major financial problems, everyone dumps the government’s currency. No one wants to hold it when they collapse and, say, decide to stop recognizing their own currency, issuing some other currency instead. That’s an extreme case, but it happens and it highlights the link between the “value of the government” and the “value of a currency”. The degree to which current inflation is a reflection of concerns about the future value of some governments is an open (and fascinating) question.

The US looks like it’s turning around. Our economy is still slowing, I think, but unemployment seems okay for now. I’m skeptical of those numbers (see my columns here: Part I and Part II) but they at least aren’t getting worse fast. At least not yet. Let’s stay hopeful.

US inflation might be slowing. Our Federal Reserve certainly actively hit the brakes sooner than most other banks and we might be seeing inflation slowing as a result. That would be good because it would mean that the US doesn’t need to hit the monetary breaks just as the economy slides into recession. If we can skate through the next year relatively unscathed and then put our fiscal house in order, that would be great[4]. It’s totally possible.

The EU and UK are in worse shape in this regard. Their timing means they will have to radically raise interest rates, slow money growth, and possibly cut spending and raise taxes. Currently they are all doing the opposite. They are expanding government programs and subsidies, mostly to offset energy costs due in large part to their poor energy policies for many years combined with Russia’s war on Ukraine today.

The question will be whether there are still other lenders out there and how they will view the situation of each economy and government.

Let’s hope for the best. And, going forward, let’s encourage more responsible policies from the governments we ourselves elect.

[1] I’m ignoring some small other sources like seignorage revenue from the central bank, publicly owned businesses, etc. since these are generally small relative to the overall budget. If I were to be more accurate I would have written something like “95% of a government’s budget comes from taking money from its citizens”. For large, developed economies all these things are maybe 5% of the total budget and also very hard to increase or decrease quickly, unlike taxes.

[2] Quote is from Prof. Guillermo Calvo’s paper “Capital Flows and Capital Market Crises: The Simple Economics of Sudden Stops” in the Journal of Applied Economics, Vol.1, No.1, 1998.

[3] The 137% is the total debt to GDP. The 97% is if you exclude what the US central government owes to other US government agencies. Either way, it’s high. Here’s a link to a graph I made, if you want to see it: https://fred.stlouisfed.org/graph/fredgraph.png?g=WA4B

{kind=link}

[4] I don’t want to always be so negative, but if you want a heart stopper, go look at our own Congressional Budget Office’s report on the long term budget. See page 5 of the PDF: https://www.cbo.gov/system/files/2022-07/57971-LTBO.pdf